Author Archives: Amanda Wiggins

April 22, 2020 2:37 pm

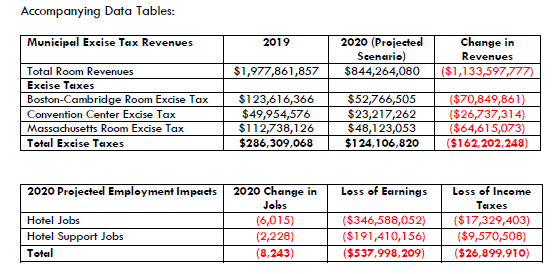

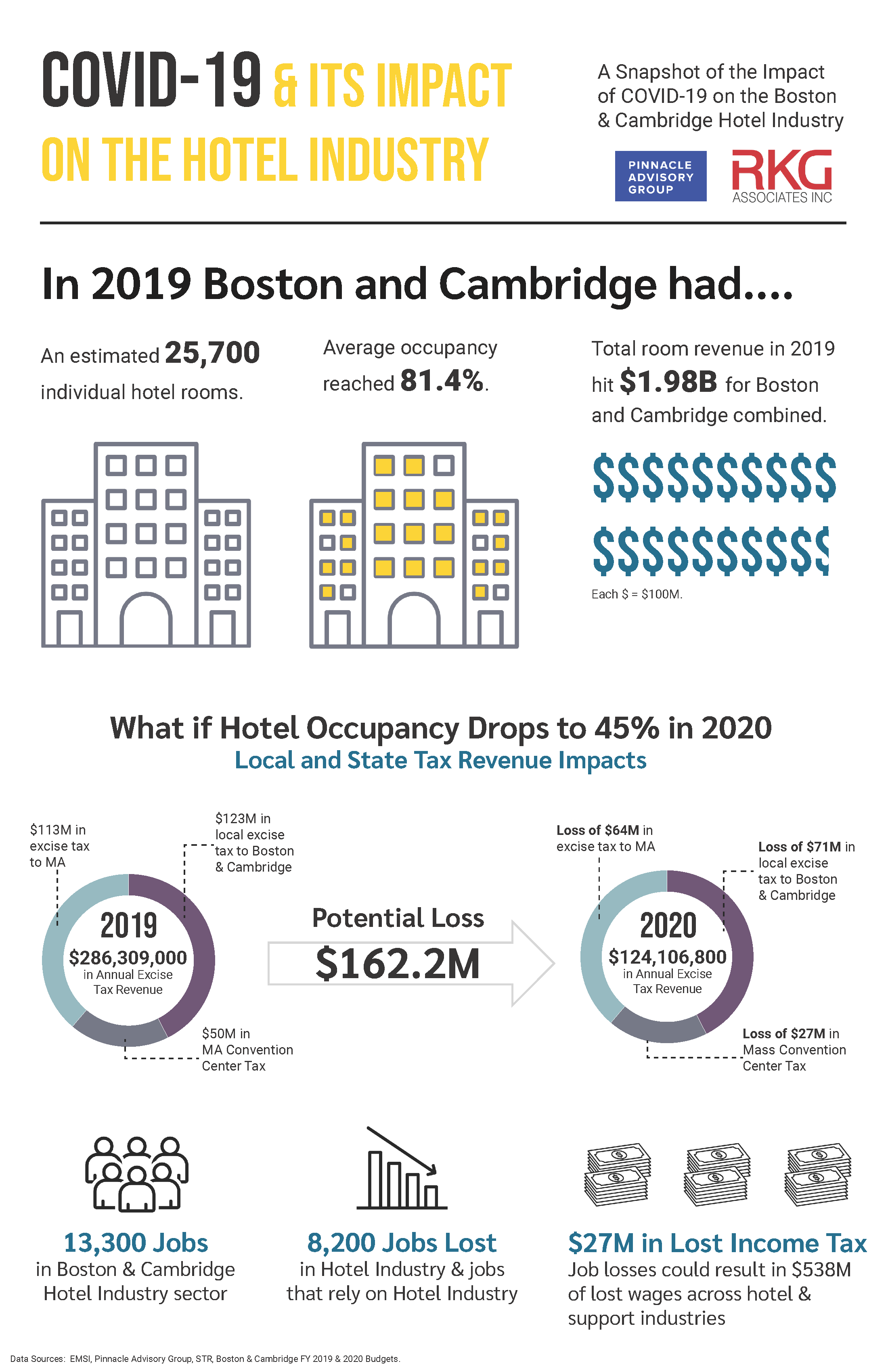

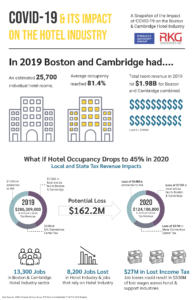

Comments Off on Impacts of COVID-19 on the Boston and Cambridge Hotel Industry – By RKG Associates and Pinnacle Advisory Group For 2019, Pinnacle Advisory Group estimated that Boston and Cambridge hotels generated nearly $2 billion in rooms revenue, based on a total supply of nearly 25,700 rooms, an average occupancy of 81.4 percent and an average daily rate (ADR) of $259. Over 13,300 people are employed in the hotel industry sector in Boston and Cambridge. Due to the pandemic and the stay-at-home requirements starting in March of this year, demand for hotel rooms has dropped precipitously, with many hotels closing completely and others only renting rooms to essential workers, often at discounted rates.

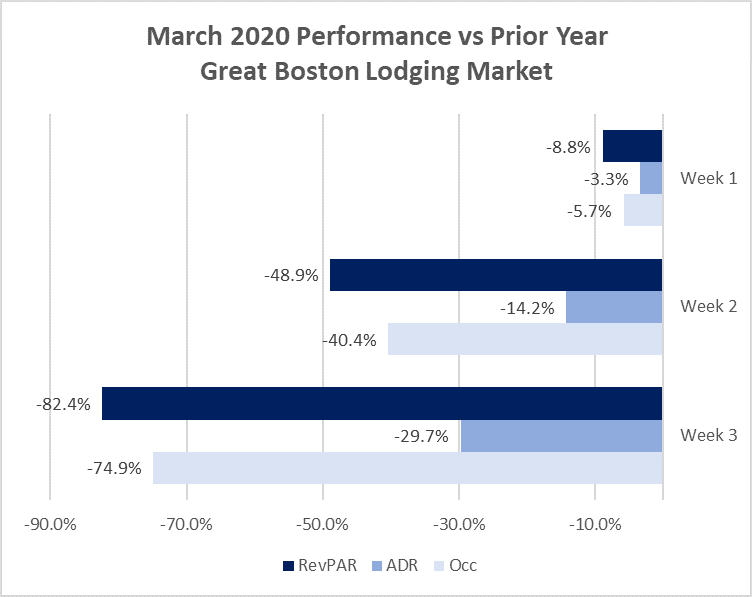

According to the Pinnacle Perspective, Revenue Per Available Room (RevPar) declined 66% for March 2020 as compared to the prior year. Hotel occupancy for March 2020 dropped to 30%, and when compared to March 2019 is a decrease of over 50%. Hotels in the Back Bay recorded the lowest average occupancy in the Boston/Cambridge market at 24% for March 2020. We anticipate further declines in occupancy and RevPar in April and May while business and leisure travelers stay at home and most hotel remain closed.

To estimate the economic impacts, Pinnacle and RKG Associates assumed a worst-case scenario where the annual occupancy rate for 2020 drops to 45 percent and the average daily rate to $200. This assumes that the economy begins to recover this summer and fall but does not regain its former strength, including a severe cutback in tourism, conventions, and international visitation – a mainstay of the city’s hotel industry. These impacts were analyzed using EMSI, a leading econometric modeling tool, to determine the direct, indirect, and induced impacts on the two cities and the region’s economy.

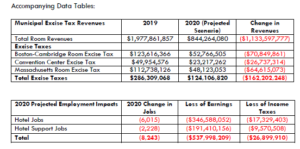

Under this scenario, hotel revenues decline by over $1.1 billion and 6,000 hotel jobs would be lost. Additionally, we estimate another 2,200 jobs in industries that support the hotel sector would also be impacted, resulting in a total of $538 million in lost wages. This in turn would result in a loss of over $27 million in state income taxes. Massachusetts room excise taxes would decline by $64 million, while Boston and Cambridge would lose nearly $71 million in local option rooms tax. The rooms tax comprises 2.8% of Boston’s annual budget and 2.3% of Cambridge, a shortfall that will need to be made up somewhere else. The Convention Center tax, which at 2.75 percent of room sales goes to support the Massachusetts Convention Center Authority, would lose $27 million.

While a 45 percent drop in occupancy levels over last year may seem extreme, it is not out of the question, given the length of time it is taking to get the economy back on track, and the longer term impacts the pandemic will have on business and tourism.

To enlarge, click on image below:

Working closely with Pinnacle Advisory Group, a leading hospitality industry consulting firm, RKG Associates analyzed the potential impacts of the current pandemic on the hotel industry in Boston and Cambridge.

To enlarge, click on image below:

About our authors:

Craig Seymour and Eric Halvorsen, AICP are Principals with RKG Associates. RKG is an economic, planning, and real estate consultancy with offices in Washington, DC, Boston, Atlanta, Dallas, and Durham, NH. Since its founding in 1981, RKG has built a track record of sound planning advice rooted in data, creativity, and realistic, implementable strategies. RKG’s strength is in a diverse range of experiences that have helped hundreds of cities, towns and private firms make the most of spaces that matter to them. RKG specializes in economic analyses, market studies, financial forecasting, strategic planning, feasibility analyses, real property valuations, and housing strategies. www.rkgassociates.com

Rachel Roginsky, ISHC, is the Owner and Principal of Pinnacle Advisory Group. Ms. Roginsky has more than 35 years of experience in hospitality consulting. Since 1991, Pinnacle Advisory Group has provided advice and analysis on the full spectrum of hospitality properties throughout the US and Caribbean: hotels, resorts, conference centers, mixed use projects, convention centers and exhibition centers. Pinnacle’s services include development counseling, appraisals, acquisition due diligence, asset management, workouts, and litigation support. Our clients include leading lenders/investors, hotel companies, universities, and municipalities. We specialize in providing personalized advice on complex projects, carefully tailoring our services to each client’s individualized needs.

April 15, 2020 4:47 pm

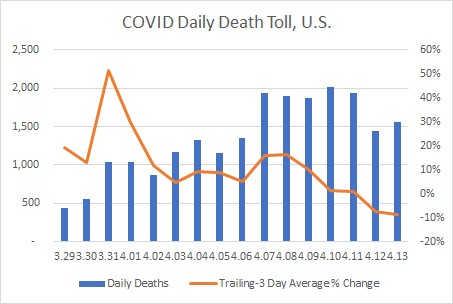

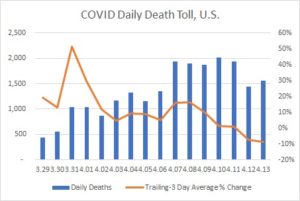

Comments Off on The Curve Has Flattened; What Does the “Interim Normal” mean for Hotel Operations? – by Karen Johnson, ISHC, MAI, CRE Though the arc of people with confirmed cases of Covid-19 is going up as more individuals are tested, the curve of the average daily death toll appears to have flattened. Which indicates that the act of social distancing will keep our ICU capacity from being overwhelmed as it was in Hunan and Italy. We can only hope.

click on image below to enlarge:

Source: Johns Hopkins University, as reported in the Wall Street Journal and the LA times

Assuming the US can get enough testing capacity to determine the true infection and mortality percentages, and plans are devised to move equipment where it is needed, things could get back to the “new normal” or at least an “interim normal” fairly soon.

There is much speculation as to when we will re-open the economy as well as on possible second waves, as happened in Toronto after the first SARs outbreak. Until a vaccine is found, infection rates will likely increase when lockdowns are rolled back. Countries about to lift lockdown restrictions are staging re-openings that put hotels and then conventions/meetings at the very end of the list. Most hotel owners cannot afford to wait.

The US hotel industry has offered to house first responders, provide additional beds for non-critical, non-communicable patients, recovering Covid-patients, and even the homeless. Thankfully, very little assistance has been required in those areas.

How do hotels create opportunities aligned with keeping society safe while still reviving our businesses?

What if US hotels focused on quarantine-safe re-integration efforts? Some households have both vulnerable and non-vulnerable members. What if hotels offered a low-cost or government-subsidized “safe haven” extended stay lodging in which vulnerable cohorts were only admitted after testing negative? For those too frail to leave home but with family members that need to be out in the world, other hotels could offer transient lodging with “in-and-out privileges” to spare that cohort the fear of bringing the virus home. Yes, families would be split, and visiting would happen across plexiglass shields. Not ideal, but neither is destroying families thru economic ruin. Now is the time for hotels to plan for the “interim normal” while social distancing is here to stay.

April 7, 2020 7:05 pm

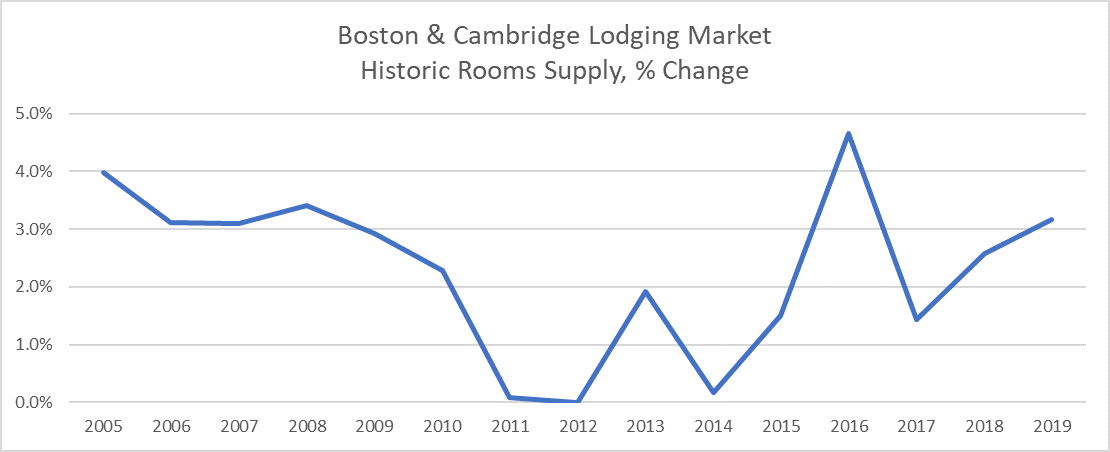

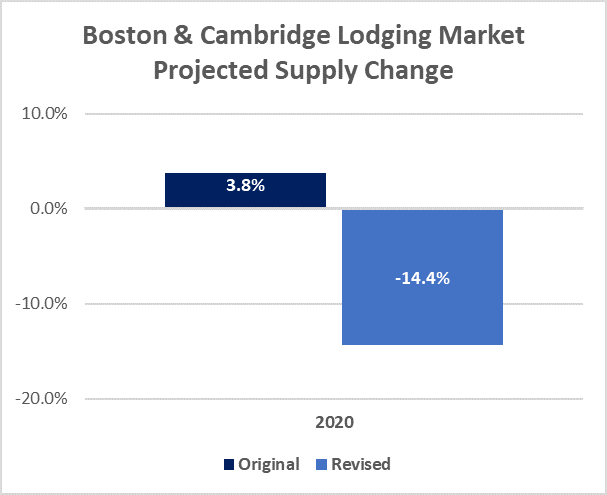

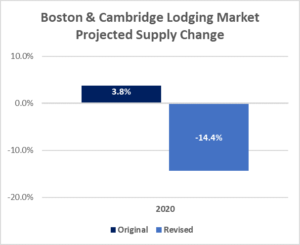

Comments Off on Boston & Cambridge Lodging Market: COVID-19 and its Impact on Supply – by Sebastian Colella Pinnacle has revised projections for 2020 supply change in the Boston & Cambridge lodging market from +3.8% to now -14.4%.

Life across the United States has changed dramatically in the last four weeks. In Boston, and almost every other city in the country, hotel owners and operators have been forced to make the difficult decision to close temporarily while the country attempts to slow and contain the spread of COVID-19. In Massachusetts those decisions were partially made for them on March 31st.

Governor Baker extended his order closing non-essential businesses in Massachusetts through May 4th. This extension included changes to operating guidelines for hotels, motels and short-term rentals which can now be used for limited purposes only; housing front-line workers fighting the coronavirus, essential workers, or residents displaced from their homes. A number of the hotels in the market, primarily those in close proximity to the city’s major hospitals, have remained open to accommodate patients and first responders. The vast majority of hotels in Boston and Cambridge, however, have closed or are in the process of closing.

History tells us that many of the hotel projects that are in planning will be delayed or may not come to fruition. For example, following the 2008/2009 recession, many hotel construction projects were stalled while others were unable to attain the financing needed to begin. Supply increased in 2009 and 2010 as projects had already begun prior to September 2008 however, there was very little growth in supply 2011 and 2012. For the four years between 2011 and 2014, approximately 300 new rooms were added to the Boston & Cambridge lodging market. In the last five years, between 2015 and 2019, the market added over 3,200 new rooms. As reported by Pinnacle previously, the surge in supply has had a mitigating effect on the market’s occupancy and rate in recent years.

click on image below to enlarge: Source: STR, Pinnacle Advisory Group

As of March 31st, the Boston Planning and Development Agency and the Cambridge Community Development Department had a pipeline made up of over 8,000 proposed hotel rooms, of which 31% are listed as under construction and over 40% are approved. Based on this construction pipeline and our familiarity with each project, Pinnacle had projected hotel supply in Boston & Cambridge to increase 3.8% in 2020. Six hotels with almost 1,000 new rooms were scheduled to open in 2020, along with the considerable number of rooms coming online from Q3 and Q4 of 2019. When including the reopening of both The Taj (reopening as The Newbury) and the Langham Hotel, the market was expected to experience its third consecutive year with above average supply growth.

Given the dramatic changes to travel that are currently taking place, the Boston & Cambridge lodging market, like many throughout the country, will experience changes not just to demand and average daily rate but its rooms supply as well. There is still much to be learned about the coronavirus pandemic and its long-term impact on the global economy. Epidemiology experts have varying opinions on the ‘best-case’ scenario however some have indicated that the country may see a retraction in the number of COVID-19 cases in the summer which would allow for a lifting or easing of travel and meeting restrictions. Under the assumption that this takes place in mid to late June, Pinnacle has revised projections for supply change in the Boston & Cambridge lodging market to decline 14.4%.

click on image below to enlarge: Assumes a retraction in the number of COVID-19 cases and a lifting of travel and meeting restrictions in mid to late June.

Source: Pinnacle Advisory Group

Supply is estimated to have declined between 15% and 20% in March with declines expected to deepen further in April reaching 80% to 90%. Most hotels which have closed have loose plans to reopen mid to late May, but even then, we do not expect that they will be operating with a full inventory of rooms. We have projected supply to return close to prior levels by August, however, we have already been notified of some hotels not reopening in 2020 but instead focusing on renovation and repositioning efforts.

Prior to the ongoing COVID-19 crises, the Boston/Cambridge market was expected to see supply increase 6.6% in 2021, the largest annual increase in rooms supply in over 20 years. A large portion of this increase in rooms was to be driven by the 1,055-room Omni Boston Seaport, the market’s largest hotel to open since the Marriott Copley Place opened in 1984. Given the declines in supply resulting from temporary closures in Q1 and Q2 2020, the supply increases expected in 2021 will be substantially greater, although somewhat artificially inflated due to the unprecedented number of temporary hotel closings.

As was the case following the financial crisis in 2008, there is expected to be limited lender interest and equity dedicated to new hotel projects as the economy faces declines. As such, hotel projects which are currently in the planning process will be delayed as financial parties wait to see how the economy responds to the COVD-19 crises and economic downturn. Following a considerable increase in supply in 2021, we expect supply increases to diminish between 2022 and 2023.

March 24, 2020 8:36 pm

Comments Off on Boston & Cambridge Lodging Market: Coronavirus Causing Steep Demand Declines Closures, Layoffs – by Sebastian Colella As travel across the country and the world has all but stopped the last few weeks from the threat of COVID19, hotels across the country saw an unprecedented amount of cancellations. The Boston lodging market has been one the hardest hit markets in the United States with demand declining dramatically throughout most of March.

Going into the year, owners and operators were worried about increases to supply, estimated at 3.8%, but looked forward to an approximate 25% increase in convention related roomnights and four additional citywides at the city’s two convention centers. Following a weak Q4 performance experienced in 2019, this year was expected to be somewhat of a correction despite the threat of new supply. In January, Pinnacle Advisory Group projected demand to increase 2.5%, its fifth consecutive year with demand growth of over 2.0%.

The Boston & Cambridge lodging market began 2020 in a good position. Accommodated roomnights in January and February increased 8.7% and 5.5%, respectively, helping to increase revenue per available room (RevPAR) 5.8% through February. March is typically the market’s first month in the calendar year with high demand levels and has averaged over 80% occupancy the last ten years. Unfortunately, the market’s positive performance in February is likely to be the last one like it for quite some time.

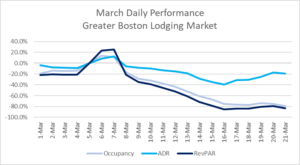

Although data for Boston and Cambridge is unavailable at this time, the declines experienced throughout the Boston MSA as reported by STR are alarming. Outside of increases on March 6 and 7 driven by an event held at the Hynes Convention Center, every day of the month has posted declines in both occupancy and ADR.

click on the image below to enlarge:

There are three primary reasons why the market has been so vulnerable to the impacts of this spreading virus in a matter of a few weeks.

- Massachusetts experienced swift spreading of COVID19 beginning March 10 and was one of the first states to declare a state of emergency, quickly disrupting businesses. There were 50 cases reported by March 10, two days later the number of cases had more than doubled and Governor Baker acted quickly requesting assistance from the federal government. On March 13, gatherings of more than 250 people were prohibited and the following day a variety of executive orders were put in place to lock down much of the State’s social activity including closing schools, restaurants and bars, banning gatherings of more than 25, and restricting visitors to assisted-care facilities. By March 23, non-essential businesses in Massachusetts were ordered closed and President Trump had extended the gathering size to a limit of ten people.

- On January 31, President Trump banned all foreign nationals from entering the US if they were in China the prior two weeks. On March 11, the President banned all travel from 26 European countries. These changes to global travel had immediate impacts on markets with international airports like Boston which has grown as an international destination over the last ten years. Adding over twenty new international destinations and completing a 400,000 square foot expansion to its international terminal, Boston Logan International Airport has more than doubled its international traffic the last ten years, increasing 125% since 2010. According to the Greater Boston Convention Visitors Bureau, the market welcomed close to 3 million international visitors in 2019.

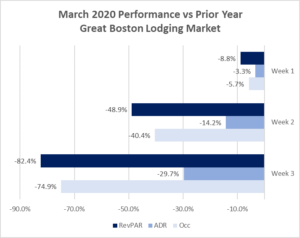

- With restrictions on meetings and gatherings in place, and the guidance on social distancing, group demand was impacted immediately. On average, 30% of the market’s accommodated demand in March is made up of group-related demand, defined as rooms booked 10 or more at a time, often related to in-house events and the City’s two convention centers. Plans for two citywides in early March representing over 31,000 roomnights were quickly changed; the International Antiviral Society’s event at the Hynes was held virtually, the Diversified Communications Seafood Expo was postponed. To date, a growing list of events have now been cancelled or postponed through June.

Every market is impacted differently by one-off events which negatively impact travel. Historically, when demand has declined considerably due to such an event, group demand is the first segment to feel it. As such, many luxury and upper upscale hotels, the full-service hotels which rely on this segment most, experience declines in occupancy. Since group demand is booked years in advance and typically at lower rates, average daily rates (ADR) is not as impacted in the short-term. As transient demand, normally the higher rated segment, begins to decline, occupancy declines at a rapid pace, negatively impacting both occupancy and ADR. Further, in an instances such as this, where travel is being restricted from international destinations, airport markets or submarkets are often negatively impacted more so than other market types. As can be seen in the below chart, while the performance for both occupancy and ADR got progressively worse each week, declines in occupancy greatly outpaced ADR.

click on the image below to enlarge:

Many hotels in Boston are now operating with single digit occupancy, forcing operators to layoff, furlough, and reduce hours of their workforce. According to Paul Sacco, President of the Massachusetts Lodging Association, 17,847 direct hotel-related jobs and over 66,799 jobs that support hotels in Massachusetts have been cut due to the outbreak. The number of hotels in Boston and Cambridge that have made the difficult decision to close temporarily continues to grow and currently represents over 20% of the market’s total rooms supply. The full-service hotels which have remained open are taking steps to trim operations to a more select-service model. Owners and operators are managing a dire situation without any indication of when it could end.

As outlined, the negative ripple effect of COVID19 has hit the Greater Boston lodging market dramatically as a result of its early spread in the State and the government’s swift reaction which included restrictions to travel and meetings, and ultimately closures of businesses. The market’s heavy reliance on group demand and its base of international travelers have contributed to the market’s decline, one that has been more severe and immediate than the aftermath of September 11th and the financial crisis in 2008. Boston typically thrives in the spring due to an uptick in leisure travel driven by its college and universities, its citywide events, the start of Red Sox Season and the Boston Marathon, all of which will materially change in the coming weeks and months.

Based on an analysis of the impacts resulting from the September 11 terrorist attacks in 2001 and the financial crisis of 2008, two events which triggered recessions, we believe the impacts of COVID19 could be felt throughout the market for years to come. There are many unknowns at this point in time and much of the impact from COIVD19 will be related to the United States and Massachusetts government’s ability to mitigate and contain the spread of the disease while simultaneously promoting a healthy economy.

January 13, 2020 4:52 pm

Comments Off on Maximizing Your Relationship With OTAs – By Tim Lee The relationship between hotels (particularly major international brands) and Online Travel Agencies (OTAs) may sometimes seem an uneasy alliance. Major hotel companies, such as Hilton, Marriott and IHG, are adding policies on price match guarantees to encourage direct bookings and detract from the perceived value of OTAs. Meanwhile, OTAs push even harder for competitive pricing and invest hundreds of millions of dollars in Search Engine Marketing (SEM) to increase their market share.

Due to acquisitions and mergers over the last two decades, most OTA brands are a part of, or work with the two largest players in the space: Booking Holdings & Expedia Group. This may come as a surprise to many hotel operators and managers, who are used to seeing reservations come in for dozens of different OTAs.

As a result of this consolidation, it appears that OTAs have gained market share and bargaining power in order to compete more effectively against branded “direct booking” campaigns. This has resulted in disputes constantly being worked out in short-term agreements between the hotel companies/brands and the OTAs. As such, the OTA strategies a hotel can or cannot engage in continuously change and can be confusing for GMs or Revenue Managers.

Beyond providing feedback on the rules of engagement to their respective brand, there is very little a branded hotel or group of hotels can do to influence the terms of OTA web marketing. Frustration regarding the terms of engagement is one of the most common friction points in the OTA-Hotel relationship, and it can prevent hotels from taking advantage of some of the free tools and services that OTAs offer.

Some hotels would prefer to do business 100% direct, and in an ideal world, that might be possible. In the interim, there are market inefficiencies and shortfalls in brand platforms that will necessitate online centralized marketplaces for lodging, where bookers can easily compare options across brand, and bundle their experiences with other travel components, such as flights or rental cars. OTAs are an important part of a hotel’s business mix in the modern age.

In these circumstances, the most productive thing a hotel can do is engage with OTAs in a mutually beneficial way and exert control over their marketing/revenue management strategy. in this article, we offer three ways hotels and hotel groups can take advantage of working with OTAs.

- Establish a relationship with your account manager:

A working relationship will help hotel management navigate and understand the ever-changing landscape of the back end of OTA platforms, and how they’re allowed to interact with your hotel. For example, the OTA can provide training materials and support for hotel staff. Additionally, an OTA account manager will have access to a host of analytical tools that they can share that will explain your market segmentation, monthly and annual performance, and identify valuable customer segments for retention.

- Keep track of analytics:

In addition to monitoring your performance, rate, and revenue produced, OTA analytics offer insights into guest segmentation. Hotels tend to view OTA room nights in the same bucket, as transient leisure business. However, most OTAs have tools that enable hotels to analyze the type of guest they send , segmented by website, country of origin, corporate vs. non-corporate, sometimes even broken down by length of stay or ADR. By identifying the highest value guests coming into the market and targeting them through OTAs, hotels are more likely to drive rate on that channel. Lastly, a hotel groups can sometimes receive portfolio level data to help with budgeting or a marketing plan, or general revenue strategy.

- Utilize flexible pricing to yield revenue:

In pursuit of ADR growth, most hotels are hesitant to provide discounts. OTAs may provide tools for attracting last minute demand and targeting specific customer segments with booking windows and higher ADRs, such as International guests or corporate travelers. While most revenue management tools are automatically designed to incentivize guests to book early and lay base business that allows them to yield rate when compression hits the market, OTAs have options on timing and segmenting price reductions, allowing savvy revenue managers to complement their existing strategies. For example- length of stay discounts, booking window discounts, timed discounts, or discounts that only appear if conditional customer segment criteria are met.

With occupancy and ADR growth slowing on a national scale, hotel management should utilize as many tools and channels as possible to continue to grow top line revenues. While appropriate discounts on OTAs can offer opportunities for upside, hotels must also understand that excessive discounting in addition to commission can represent a significant marketing cost. As the landscape surrounding the hotel company-OTA relationship continues to shift, hotels should make the best of their current situation, and leverage the tools they have available if it makes sense.

About Tim Lee:

Timothy Lee is a Consultant with Pinnacle Advisory Group, a premier, national hotel consulting firm. In his current role, he specializes in conducting feasibility analyses and impact studies. Prior to joining Pinnacle Advisory Group, Timothy worked as a Market Manager for Expedia Group, Timothy is a graduate of the School of Hotel Administration at Cornell University and is a member of the New England Chapter of the Cornell Hotel Society. Timothy is based in Pinnacle’s Boston office. Pinnacle’s knowledge and experience with OTA’s is one way that it provides value to its asset management clients and those seeking improved performance through operational reviews.

For more information on how Pinnacle might be able to assist you, please contact Tim Lee, or Rachel Roginsky, ISHC – Principal at 617-722-9916. www.pinnacle-advisory.com

October 30, 2019 4:03 pm

Comments Off on NEIRA 2019 Annual Conference Presentation – by Meri Keller Meri Keller discussed New England Lodging Trends at the New England Inns & Resorts conference on October 30, 2019.

Please click on the title below to view the presentation:

Pinnacle – NEIRA Presentation FINAL 2019

October 16, 2019 3:14 pm

Comments Off on Ninth Annual Boston Lodging Pulse and Market Insights – Rachel Roginsky, ISHC Rachel Roginsky, ISHC presented at the Ninth Annual Boston Lodging Pulse Event. Her discussion included data on a national level with a focus on the Boston and Cambridge Markets.

To view the presentation, please click on the link below:

Pulse 2019.final

September 5, 2019 6:55 pm

Comments Off on Rhode Island Hospitality Economic Outlook – by Rachel Roginsky, ISHC Click on the title below to view the presentation:

Rhode Island Hospitality Presentation

August 6, 2019 3:06 pm

Comments Off on Outlook 2020 – Rachel Roginsky, ISHC Click on the title below to view or download the Outlook 2020 presentation given by Rachel Roginsky, ISHC for the Mass Lodging Association:

FINAL – Outlook 2020

July 21, 2019 7:28 pm

Comments Off on The Boston Lodging Market: What the Supply Surge Means Moving Forward – by Sebastian Colella At year-end 2018, the Boston and Cambridge lodging market was comprised of 105 hotels with approximately 24,000 rooms. While this has grown considerably in four years, lodging supply in this market remains small relative to other major gateway cities. The ongoing building boom in Boston and Cambridge has contributed greatly to the recent surge in lodging supply and is expected to continue through 2021 and beyond.

What does the pipeline of hotel development, its largest in recent history, mean for the Boston lodging market’s performance?

Recent & Continued Supply Growth

Between 2000 and 2014, rooms supply in market increased at an average rate of 2.3% annually. As financing became more readily available and market dynamics continued to improve, hotel projects began moving forward. Between 2015 and 2018, over 2,600 rooms opened in the Boston lodging market, a 12% increase in just four years with the largest increases experienced in 2016 and 2018.

Despite these above-average increases to supply, demand has kept pace. Market occupancy has remained above 80% for six years, reaching a historic high of 82.7% in 2018. Much of this demand growth is a result unaccommodated demand previously forced to stay elsewhere due to lack of availability, specifically weekdays throughout most of the year and weekends May through October.

To Read the Full Article, Click on the Article Title Below:

Boston Lodging Market 8.2019 – Sebastian Colella