Boston & Cambridge Hotel Market Reaches Historic Highs in 2017 Before Next Wave of Supply – by Sebastian Colella

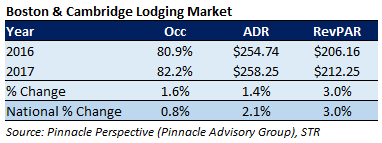

Mirroring the US national lodging market’s eight straight years of demand growth, the Boston and Cambridge lodging market recorded an occupancy of 82.2% in 2017, its highest in history. Average daily rate (ADR) increased 1.4% to $258, another market record. Driven more by occupancy than rate, the resulting market revenue per available room (RevPAR) increased 3.0%, matching the growth experienced nationally in 2017. Although the market’s RevPAR declined in 2016 for the first time in six years, dynamics shifted in 2017 as the market benefitted from a strong convention calendar with well-placed citywides, continued increases to both corporate and leisure demand, and a slowing of supply growth.

The U.S. economy had a solid 2017 as unemployment declined to its lowest point in 17 years, GDP growth improved, and the stock market reached record highs. In addition to positive momentum in the national economy, many of the local elements which typically contribute to the success of a hotel market drove demand to its record high level in 2017. The Greater Boston Convention & Visitors Bureau has reported that Boston had an all-time high 1.7 million international visitors in 2017, up 5.3% over 2016. Through September of 2017, domestic traffic through Boston Logan International Airport increased 4.7% while international traffic increased 10.7% compared to the same period last year. Primarily a result of the airport’s ability to launch new international routes, the airport was pacing to surpass 38 million passengers for the year. According to the Massachusetts Convention Center Authority, the Boston Convention and Exhibition Center and the Hynes Convention Center achieved record setting results in hotel room night production in 2017 accounting for a total of 665,965 room nights, a 10% increase to the prior year. Lastly, the office market fundamentals remained strong in Boston and Cambridge in 2017 with 1.1 million square feet of positive absorption and a vacancy rate of 9.0% according to Colliers International.

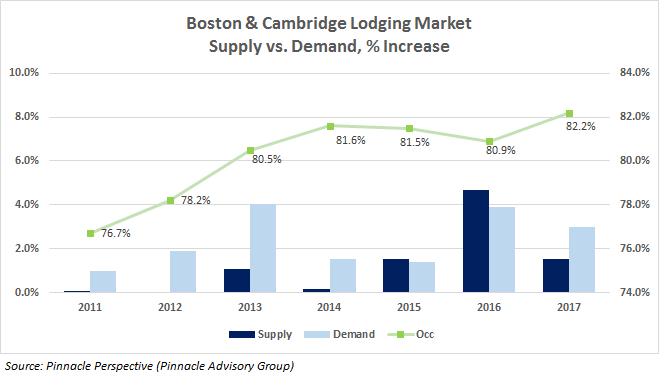

While macroeconomic issues facing the nation’s economy, the market’s convention calendar, and seasonality/holidays can influence the local market’s occupancy and ADR, nothing seems to play a greater role than fluctuations to lodging supply (available rooms). Similar to many markets throughout the country, the economic environment following the 2008/2009 recession led to very little growth in supply growth for years helping to improve market performance. Eight hotels combined for approximately 1,400 rooms opened in Boston and Cambridge in 2015 and 2016, increasing the market’s supply 1.5% and 4.7% respectively. Although demand growth was strong both of these years, it did not keep pace with supply causing occupancy to decline slightly each year. The positive dynamics of 2017, however, increased demand 3.0%, growing the market’s occupancy from 80.9% to 82.2%, its largest increase since 2013.

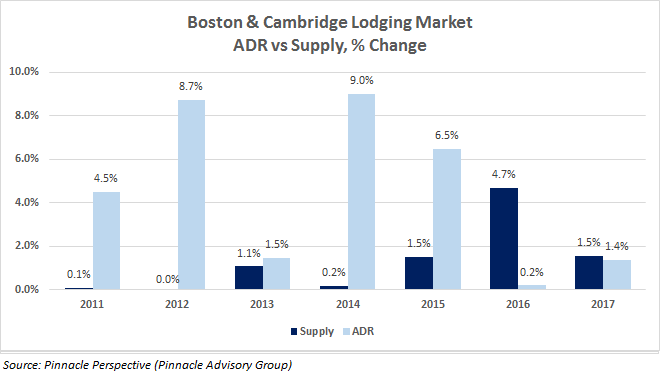

As supply increases the concern lies most with market ADR growth, which has decelerated to below inflationary levels the last two years. There are many factors which can impact a market’s ADR however over the last seven years, with the exception of 2015, there does seem to be a correlation of supply fluctuation to ADR growth. As supply increases, existing properties are often times forced to price more competitively, especially during lower demand periods. Additionally, most of the market’s new supply the last three years has been select-service, positioned below many of the market’s full-service hotels, and in most cases offering lower introductory room rates. Three of the four years in which supply increased over 1.0%, ADR increased below 2.0%. Conversely the three years with supply remaining relatively flat, ADR increased between 4.5% to 9.0%.

There is a pipeline of hotel projects representing higher than average supply growths for the Boston and Cambridge market over the next four years. Historically, Boston has not seen significant increases to its supply in the form of a “boom” but rather small increases over time. This is primarily due to lack of available land, high development and operating costs, and an ADR (top line revenue) that, in most cases could not justify the cost to build. While these factors still exist today, the higher revenue forecasts have enabled developers to underwrite more feasible projects.

A slate of new supply will enter the market in 2018, much of it consisting of smaller, select service hotels. Combined with expansions of existing hotels, the addition of over 1,100 new rooms to the local market will increase available rooms supply in Boston and Cambridge over 3.0% in 2018.

The Boston Planning and Development Agency combined with the Cambridge Community Development Department have a pipeline made up of over 7,500 proposed hotel rooms, of which 1,700 are listed as under construction and 4,100 are approved. Above average supply growth will continue in 2019 with available rooms supply expected to increase over 4.5%. Hotels expected to open next year include the Cambria Hotel in South Boston, the Moxy Theater District, the Four Seasons Back Bay, the CitizenM North Station along with the potential for other smaller projects with shorter development timelines to move forward.

Boston’s economy is driven by a diverse set of growth engines which provide it with a level of stability over the long-term. The area’s rich history, amenities, and ease of access contribute to its ability to attract group and leisure travel. While the market remains reliant on its traditional industries such as financial services, education and healthcare, it has also become a hub for innovation, technology, and life sciences all of which drive corporate travel throughout the calendar year. Economic indicators for the overall Boston and Cambridge lodging market are positive and illustrate the underlying strength of the broader market. Demand growth is expected to continue at a similar pace assuming broader economic trends remain favorable. While most proposed hotel projects will induce new and unaccommodated demand into the market, increases to supply at the levels projected for the next three to four years will mitigate ADR growth. While occupancies are projected to remain above the long-term average (76% occupancy), growth in ADR will fluctuate with increases to supply but over the long term will be in line with long term Consumer Price Index in the Boston-Cambridge area of 2.4%.

* * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * *

Sebastian Colella is a Vice President with Pinnacle Advisory Group’s Boston office completing assignments in urban and suburban markets throughout the country with primary responsibilities covering the firm’s work in Boston and Cambridge. Sebastian holds a Bachelor of Science degree from the School of Hotel Administration at Cornell University with industry experience in hotels, resorts, and private clubs.

About Pinnacle Advisory Group

Since 1991, Pinnacle Advisory Group has provided advice and analysis on the full spectrum of hospitality properties throughout the US and Caribbean: hotels, resorts, conference centers, mixed use projects, convention centers and exhibition centers. Pinnacle’s services include development counseling, appraisals, acquisition due diligence, asset management and litigation support. Our clients include leading hotel companies, REITs, universities, major banks, and municipalities. We specialize in providing personalized advice on complex projects, carefully tailoring our services to each client’s individualized needs.