Boston & Cambridge Lodging Market Takes a Positive Turn in Q3 – by Sebastian Colella

Following a weak second quarter which featured monthly declines in occupancy and rate declines in both April and May, the Boston & Cambridge lodging market bounced back in the third quarter driven by considerable demand and average daily rate (ADR) in August and September. A solid base of group demand helped to increase compression and drive transient rates during both months, positioning the market to end the year with RevPAR growth over the year prior.

The third quarter resulted in mixed monthly results, but on a year-to-date basis there was a positive change for the market. Q3 occupancy was 91.4%, an increase of 2.9 points from Q3 2017, while ADR increased 1.1%. The third quarter’s RevPAR increased 2.1% over last year. These three months offered 39 compression nights, dates with an occupancy of 95% or higher, a considerable increase from the 27 achieved in Q3 2017.

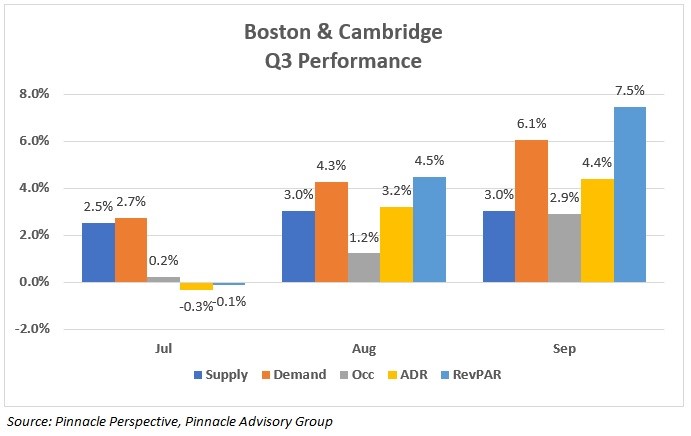

July of 2017 benefitted from a favorable convention calendar which was not the case in 2018. With an 11% decline in group demand, operators dropped transient rates in order to maintain occupancy levels. Without much growth in transient rates, the market ADR declined 0.3%, negatively impacting the month’s RevPAR. Despite the declines in occupancy, July had 15 compression nights, three more than last year.

Largely driving the increases to demand in August, group increased 10%. According to the Massachusetts Convention Center Authority (MCCA), the BCEC and Hynes convention centers generated over 51,000 roomnights in the month, an increase of over 50% from August 2017. The month included 11 nights of compression, an increase from last year’s six. Rate growth of 3.2% in the month was driven entirely by transient rates which made up the majority of August’s 4.5% RevPAR growth.

September’s 6.1% growth in accommodated roomnights marked the market’s thirtieth consecutive month of demand growth. A high level of compression in the month was created by a 15% increase in group demand, which in turn helped operators drive transient rates over 6%. The month included 13 compression nights, four more than last year, at an ADR of over $330.

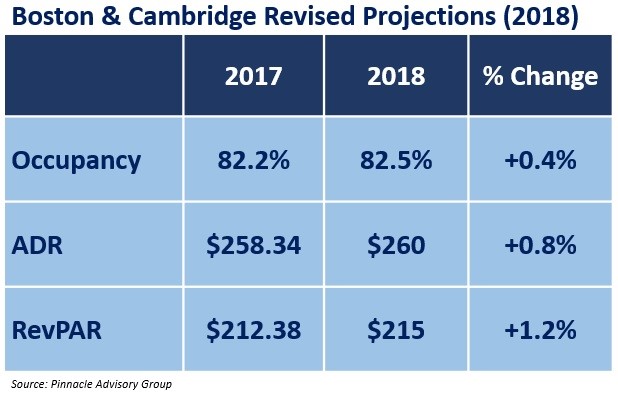

Year-to-date through September, market occupancy has increased 0.5 points and ADR has increased 0.6% compared to the same time period last year. As presented previously, market rate increased 3.2% and 4.4% in August and September, respectively, and similar rate growth is expected for October, a month which featured three citywide events at the Boston Exhibition & Convention Center and the Red Sox playoff run through the World Series. Pinnacle had originally projected the market’s RevPAR to decline 0.5% for calendar year 2018. As a result of the delays in expected hotel openings, above average increases in demand in August and September, combined with the dramatic shift in market rate growth in the third quarter, revised projections indicate a RevPAR growth of 1.2% in 2018.

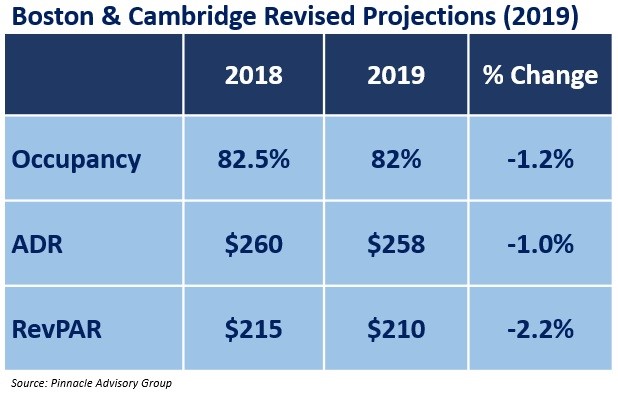

As a result of these positive shifts, Pinnacle has revised projections for 2019. Continued growth in demand of approximately 3.7% is forecasted, however it will not keep pace with supply which is expected to increase over 5%. As a result, occupancy is projected to decline to 82% in 2019 while ADR is projected to decrease 1.0%. Pinnacle is projecting a negative RevPAR in 2019, the first decline since 2016 when the market experienced a similar increase to supply. With the convention calendar indicating a decline of approximately 24% in roomnights (only three months with growth over 2018) and two less citywide events, there will be a lack of base demand to drive rate growth seen in previous years.

Pinnacle Advisory Group’s projections for the Boston and Cambridge lodging market are presented to the Massachusetts Lodging Association annually. The updated presentation can be viewed here.

Sebastian J. Colella is a Vice President with Pinnacle Advisory Group based in the Boston office. With over 15 years in the hospitality industry, Mr. Colella leverages his operational knowledge and expertise from experiences in the field. In the last three years Mr. Colella has completed over 75 hotel consulting and valuation assignments for existing and proposed hotels throughout the country with a primary focus on Boston and its suburbs.

Prior to joining Pinnacle Advisory Group, Mr. Colella held a variety of management roles in hotels, resorts and private clubs. With capacities focusing on both sales and operations, he has worked for ClubCorp, the world leader in private clubs, Rosewood Hotels’ flagship property in New York City, The Carlyle, and lead efforts to open Zanzibar, Tanzania’s first luxury resort, Baraza Resort & Spa. Work with Pinnacle Advisory Group has included market and feasibility analysis, acquisition due diligence, departmental revenue and expense performance evaluations, facility recommendations, brand assessments and impact studies, as well as appraisals of both branded and independent hotels and resorts.