Boston Lodging Market Poised for Continued Growth – by Sebastian J. Colella

The economy in Boston and Cambridge is driven by a diverse set of growth engines which have provided it with a level of stability through multiple recessions. While the city remains reliant on its traditional industries such as financial services, education and healthcare, it has also become a hub for innovation, technology, and life sciences, all of which drive corporate travel throughout the calendar year. The city’s rich history, convention centers, amenities, and ease of access contribute to its ability to attract group and leisure travel. The Boston/Cambridge lodging market has now experienced six consecutive years of revenue per available room (RevPAR) growth with very few additions to supply since the most recent recession. As a result, the area has become one of the most sought after and desirable markets in the country for investment in both new projects and acquisitions.

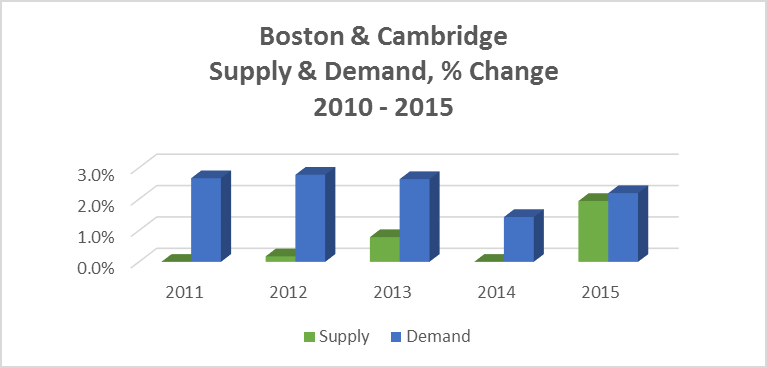

Demand Outpacing Supply

The Boston/Cambridge lodging market supply is made up of 101 hotel properties combined for approximately 23,000 rooms. Similar to many markets throughout the country, the economic environment following the 2008/2009 recession led to very little growth in supply. Between 2010 and 2015, the market welcomed seven new hotel properties of approximately 801 rooms, of which over 70 percent opened in 2015. When accounting for minor roomcount changes and expansions, the local market’s room supply has increased 0.7 percent on a compound annual basis the last six years. During this same six year period, accommodated demand has increased year after year at a compound annual growth rate of 2.4 percent.

Source: Pinnacle Advisory Group

Driven by the city’s continued demand growth across all three primary demand segments, corporate, group and leisure, and its lack of new supply, operators have been able to increase rates considerably. In 2015, occupancy in the Boston/Cambridge market increased 0.2 points to 81.8 percent with average daily rate (ADR) increasing 6.4 percent to $254.10. The resulting RevPAR in 2015 increased 6.7 percent from the prior year to $207.83, a historic high for the market.

Source: Pinnacle Advisory Group

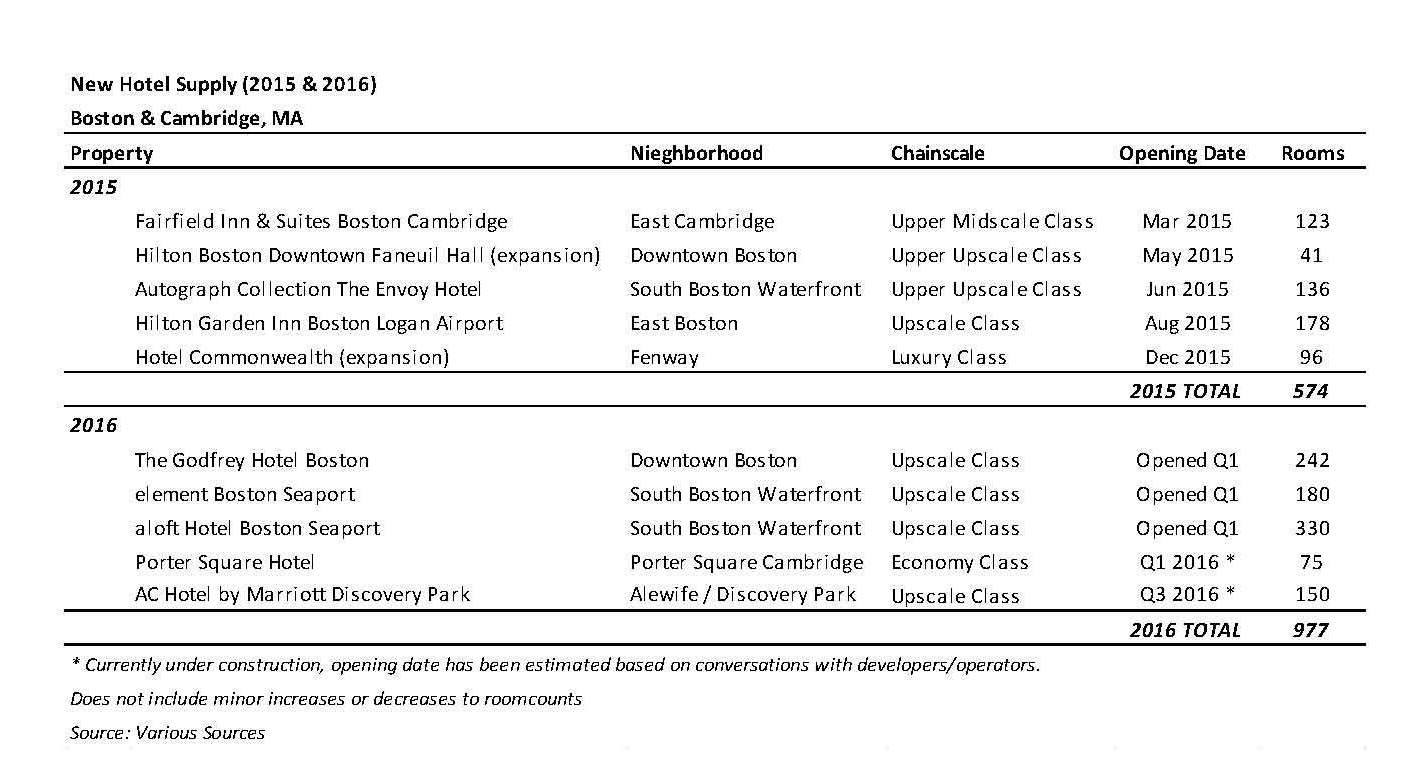

Future Changes to Supply

Historically, Boston has not seen significant increases to its supply in the form of a “boom” but rather small increases over time. This was primarily due to the area’s high labor costs, lack of available land, and an ADR that, in most cases could not justify the cost to build. Some of these factors still exist today however the recent growth across all demand segments has enabled developers to once again underwrite feasible projects.

In 2015, new supply in Boston and Cambridge was limited to three new hotel properties and two guestroom expansions, combining for a total of 574 rooms. The Boston/Cambridge market is expected to welcome five new hotels (977 rooms) this year, a four percent increase to existing supply. The market has not seen a one year increase this large since 2006 when the InterContinental and the Westin Waterfront opened adding 1,217 rooms.

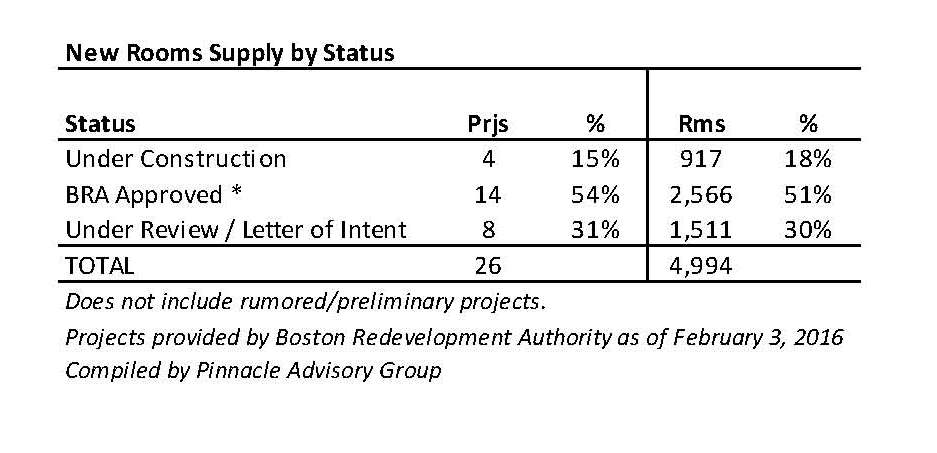

There are proposed hotels, both select-service and full-service, throughout the city with projected opening dates in 2017 and beyond, many of which cannot be confirmed as moving forward at this time. As of February 3, 2016 there were 26 hotel projects, representing approximately 5,000 rooms, in the Boston Redevelopment Authority’s (BRA) pipeline – this does not include the three hotels which have already opened this year. It is highly unlikely that all of these hotel projects will move forward, however it is a good indication of the level of interest investors and developers have in the immediate area.

The lodging market, while volatile at times, is cyclical in nature. As evidenced by the Boston/Cambridge market’s historic peaks and valleys in both occupancy and rate over the last twenty years, the local area is of no exception. While it is difficult to predict a lodging market’s exact peak, one can apply the basic stages of a real estate cycle which would indicate the Greater Boston lodging market has been in the recovery stage since 2010 and has recently begun its expansionary stage as new hotels are approved, completed and opened. It is between this stage and the oversupply stage where investors benefit most from their property’s peak real estate value. Although we are forecasting a slight decline in market occupancy, oversupply is not expected to be an issue in the immediate future given trends in demand growth.

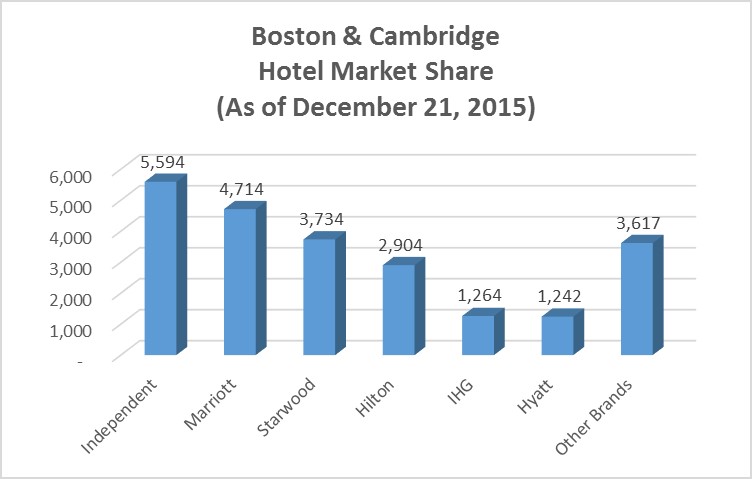

Seventy-five percent of the city’s rooms supply is affiliated with a nationally recognized hotel brand. As such, the industry’s consolidation among hotel companies striving to increase market share is another interesting way in which the city’s supply could change overtime. The 16 Marriott International properties combine for over 4,700 rooms (20 percent market share) while Starwood Hotels & Resorts represents over 3,700 rooms (16 percent). Both of these hotel companies represent a sizeable portion of the city’s group hotels, four of which are attached, or in close proximity, to the two convention centers. Hilton Hotels & Resorts represents 2,900 rooms (12 percent), while InterContinental Hotel Group and Hyatt Hotels, both having slightly over 1,200 rooms, represent approximately five percent.

Source: Smith Travel Research

Increased Acquisition Activity

Many hotel owners have sought to take advantage of the current market conditions, selling hotel assets while their top and bottom lines continue to outperform previous years. Simultaneously, many national and international investors seek to enter the Boston market known for its high barriers of entry and are willing to pay record prices for existing assets due to the market’s positive fundamentals, diverse economy, and robust demand growth in recent years.

These two driving forces have resulted in nine hotels having been reported sold in the Boston/Cambridge since November, many of which were for prices per key well above previous sale prices and at relatively low capitalization rates.

In November, Junson Capital, a Chinese real estate investor, purchased the 210-room Le Meridien Cambridge MIT. The following month, Oxford Capital sold the 242-room Godfrey Hotel, which had not yet opened at the time, to Germany-based Union Investment Real Estate. Other sales in December included the 471-room Renaissance Boston Waterfront, the 114-room Ames Hotel in downtown Boston, and the 13-room Beacon Hill Hotel & Bistro. In January, Mandarin Oriental Hotel Group agreed to exercise its option to purchase the Mandarin Oriental Boston for almost $1 million per key, the highest sale price per room of any hotel in Boston history. The Hotel Commonwealth was sold to Xenia Hotels & Resorts following its $50 million expansion which added 96 rooms and approximately 7,000 square feet of meeting space. Most recently, HHM (formerly Hersha Hospitality Management) purchased the Best Western Tria in Cambridge and the Blackstone Group purchased the 178-room Club Quarters in downtown Boston.

The Greater Boston area will continue to be one of the most sought after markets in the country, attracting both national and international investors. Properties without encumbrances, be it a ground lease, management, a flag and/or union operations, will be the driver in higher acquisition prices as buyers pursue deals which minimize risk and maximize profits.

Looking Ahead

Statistics for the overall Boston/Cambridge lodging market are positive indicators for the city’s future prospects and illustrate the underlying strength of the broader market. Pinnacle Advisory Group has projected a seventh year of increased market demand in 2016 with the city projected to maintain an occupancy level above 80 percent. Current demand trends throughout Boston and Cambridge and the market’s capacity constraints through much of the year will allow operators to continue increasing average daily rates, which are projected to be, once again, the driver behind RevPAR growth in 2016.

Despite the risk of new supply, the positive fundamentals outlined above are expected to continue as the basis for underwriting new hotel projects and maintaining a high level of investor interest. Macroeconomic issues facing the nation’s economy today such as oil prices, the US Dollar, China’s recent economic slump, the spread of the Zika Virus among others, should be monitored as they may have an impact to lodging markets across the country. In spite of these uncertainties, long term prospects for the Boston/Cambridge market are encouraging.

* * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * *

About the Author

Sebastian Colella is a Vice President with Pinnacle Advisory Group’s Boston office with assignments in urban and suburban markets throughout the country with a primary focus on Boston and its suburbs. Sebastian holds a Bachelor of Science degree from the School of Hotel Administration at Cornell University with industry experience in both sales and operations roles at hotels, resorts, and private clubs.