The Boston & Cambridge Lodging Market’s Recovery Projected to Accelerate into 2022 – by Sebastian Colella

Despite uncertainties surrounding corporate travel and the return to the office, as well as the Delta variant and the potential for mask mandates and other state or federal restrictions, the Boston & Cambridge lodging market continues to climb a wall of worry. Driven primarily by domestic leisure travel, the market has experienced strong month-over-month gains in demand and average daily rate (ADR) since March.

Click on image below to enlarge:

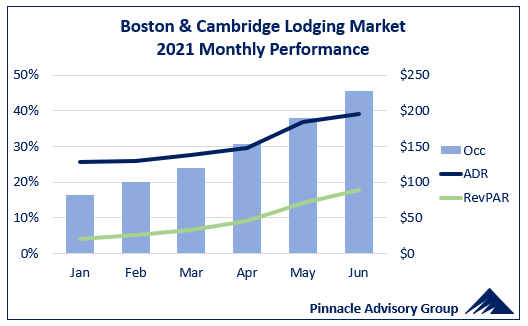

Although the market has experienced considerable gains the last three months it still lags the United States as a whole and almost every other top-25 market in recovering to pre-pandemic levels. Through June, Boston ranks as the third slowest market to recover among top-25 markets, behind only New York City and San Francisco, according to STR. The Boston & Cambridge lodging market’s occupancy was 46% in June 2021, its strongest occupancy all year yet only half of its level in June 2019. Despite month-over-month gains in ADR since January, market ADR is down approximately 38% to 2019. As a result, the Boston & Cambridge lodging market’s June revenue per available room (RevPAR) of $47 is 77% less than it was just two years earlier.

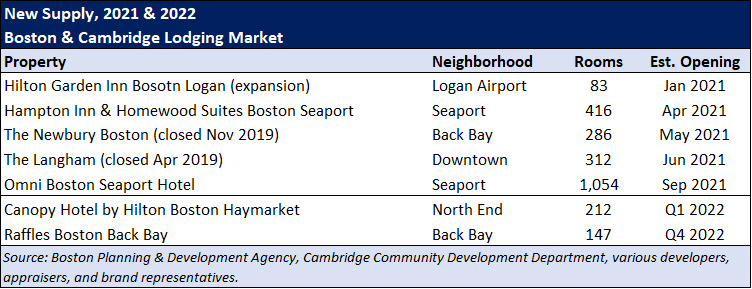

Due in part to its smaller size, the dynamics of the Boston & Cambridge lodging market have proven to be delicate as it relates to increases to its supply. In 2021, the market will welcome over 2,000 new rooms, including the 1,054-room Omni Boston Seaport Hotel, resulting in a supply increase of over 4.0%. As these rooms continue to come online in 2022, two additional hotels are expected to open increasing supply another 5.0%. Over the last 25 years, the market’s supply has increased 2.5% on a compound annual basis so back-to-back gains in supply of this size are an added headwinds the market will face as it recovers from the pandemic.

Click on image below to enlarge:

Through June, hotels have relied primarily on leisure demand with certain submarkets, such as Fenway/Longwood and North/West End, benefiting the most. There has been slow growth in business transient since the spring with notable increases in volume in July. Since the State’s reopening in May, weddings and other social functions have proven to be resilient while corporate meetings, although smaller, have started to take place in recent months. The Boston Convention & Exhibition Center and the Hynes Convention Center have numerous events scheduled between July and yearend including five citywides. When considering these trends, combined with the unique sports events being hosted this fall including the Laver Cup, the rescheduled Boston Marathon, the Head of the Charles, NCAA Fenway Bowl Game, as well as the possibility for an extended Red Sox season, the Boston market is well positioned for continued improvement into Q3 and Q4 of 2021.

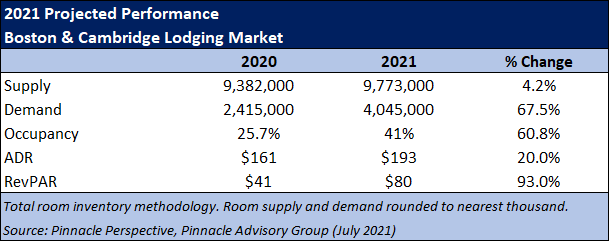

Assuming Massachusetts and the City of Boston remain without added restrictions due to a late summer or fall COVID-19 surge, Pinnacle has projected occupancy to reach 41% in 2021 and ADR to increase 20% over 2020. The resulting RevPAR of $80 in Boston & Cambridge is 37% indexed to its 2019 level.

Click on image below to enlarge:

Pinnacle has forecasted trends to continue through 2022. Corporate demand, with the exception of international, is expected to see continued growth as companies return to offices and domestic travel becomes more commonplace among larger companies. Growth in group demand is expected to outpace corporate demand in 2022. Many events from the last 18 months have been rescheduled for 2022, the convention calendar’s citywide and roomnights are comparable to 2019, and SMERF related group is expected to remain consistent. Leisure travel was the lone bright spot in 2021 and it is assumed it will remain strong through 2022 with an extended season, longer weekends, and increased length of stays. Assuming international travel begins to return in early 2022, specifically key markets such as Canada and Europe, the market would benefit from a second round of pent-up corporate and leisure demand from an international demographic.

Pinnacle has projected the Boston & Cambridge lodging market to have an occupancy of 66% in 2022 with a 22% increase to ADR. The market’s RevPAR of $155 is approximately 72% indexed to 2019.

Click on image below to enlarge:

Rachel Roginsky, Principal, and Sebastian Colella, Vice President, presented Pinnacle Advisory Group’s projections for the Boston Suburbs and the Boston & Cambridge lodging markets at this year’s Massachusetts Lodging Association’s Annual Outlook event on July 29, 2021. The full presentation can be found here.