Author Archives: Amanda Wiggins

October 7, 2020 4:23 pm

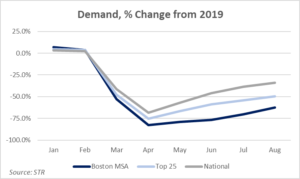

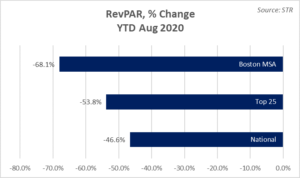

Comments Off on Through August, Greater Boston Lodging Market Ranks as the Hardest Hit by Pandemic – by Sebastian Colella The Greater Boston market has experienced a 71% decline in room revenue through August when compared to the same time last year, the largest decline of all top-25 markets according to STR. Hotels in Boston and Cambridge, as well as those in the Greater Boston area, began to feel the effects of the ongoing pandemic in early March, before many markets around the country. Declines in lodging demand showed improvement over the summer months as there was an uptick in leisure travel, however, this began to slow towards the second half of August. Despite this slight boost, lodging demand was still down 70% and 62% in July and August respectively. Having endured six months of unprecedented declines to demand and revenue through August, hotel owners and operators are concerned that the declines will worsen in the fall and winter months as leisure travel slows and corporate and group demand remain practically non-existent.

Greater Boston

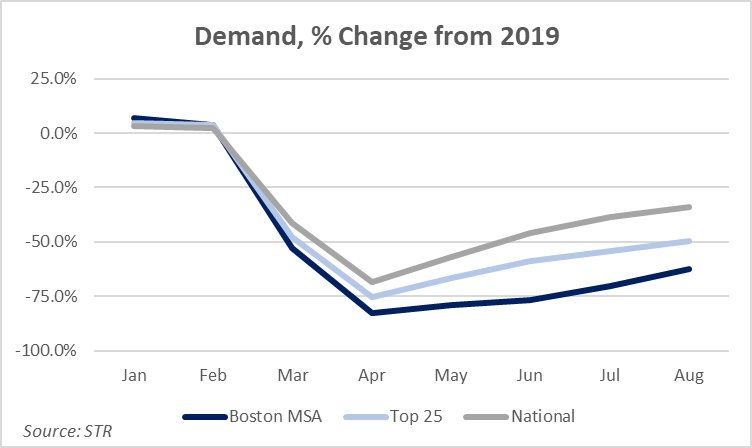

Demand declines followed a similar pattern across the Boston MSA, the country’s top-25 markets, and the country as a whole. However, the Boston MSA was more negatively impacted than all top-25 markets and the gap widened in May and June as the State managed a higher number of COVID-19 cases and in turn, applied more strict restrictions on travel and businesses, specifically hotels.

click on images below to enlarge:

Through August, revenue per available room (RevPAR) has declined over 68% in Greater Boston while the country as a whole has experienced a 47% decline. Submarkets which have endured the pandemic better than others include interstate hotels, extended stay hotels, and economy and midscale hotels. Given the make-up of the Boston hotel supply, which is mostly higher rated, full-service hotels which rely heavily on corporate and group demand, the overall market struggled more so than others.

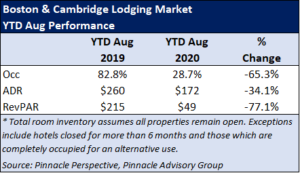

Boston & Cambridge

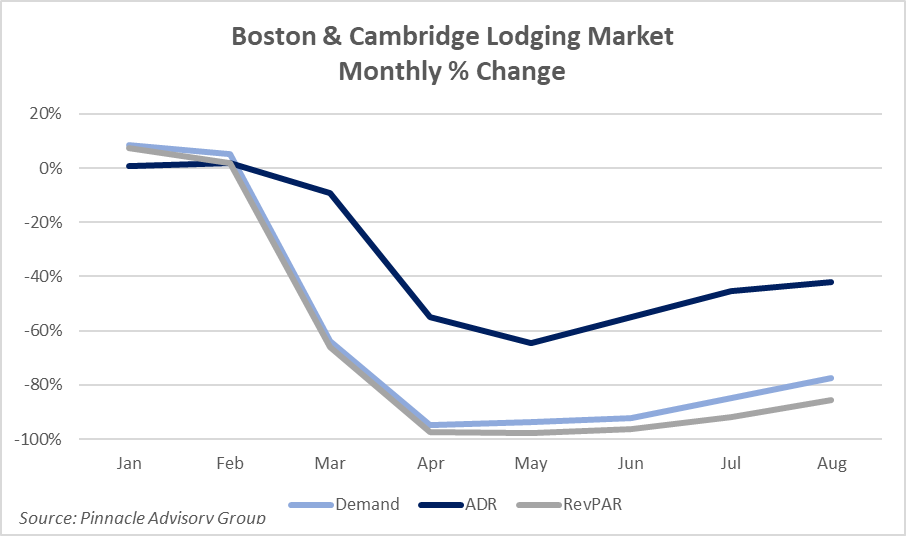

Historically, the Boston and Cambridge lodging market accommodates approximately half of the Greater Boston market’s demand annually. Year-to-date through August, Boston & Cambridge had an occupancy of 28%, down from 83% the same time last year. Average daily rate (ADR) through August was $172, a 34% discount to the same time in 2019. As a result, RevPAR in Boston and Cambridge has declined 77%.

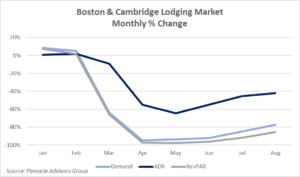

The largest declines occurred April through June as businesses managed the state of emergency orders which restricted businesses, specifically hotels ability to accommodate travellers and large gatherings. Lodging demand, or occupied roomnights, was down over 90% each month from April to June when compared to the prior year. Those declines in demand improved slightly over the summer, -85% in July and -75% in August, as regional leisure travel picked up.

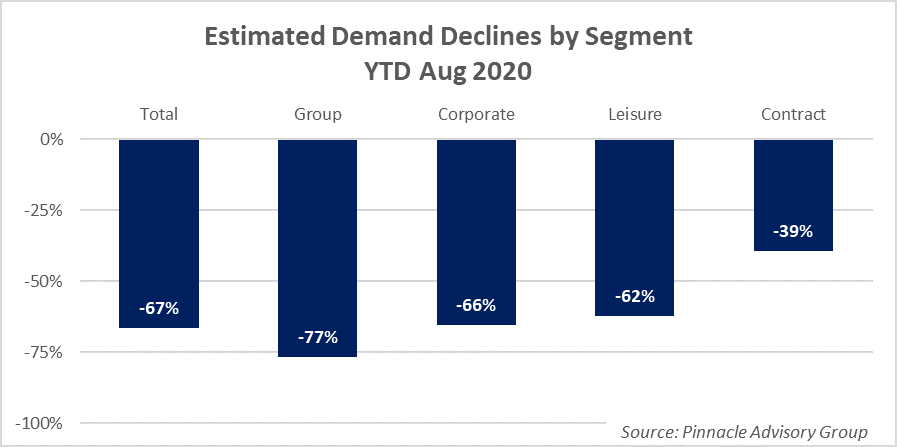

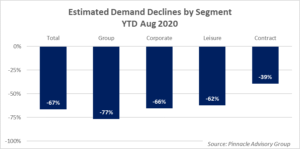

Group, corporate and leisure demand each represent between 28% and 33% of the market’s accommodated demand, combining for about 95% of its total. Through August, group demand, bookings of ten or more rooms, has seen the steepest declines, estimated at 77%. This is projected to be the slowest segment to return and has shown little recovery since declining in March. Corporate demand has declined approximately 66% through August and is projected to see a slow recovery beginning in Q2 or Q3 of 2021. Despite improvements experienced the last two months, leisure demand has declined 62% during the same period. Given the slow growth trajectory of demand and the seasonality of the market with winter months approaching, the declines by segment are expected to be more pronounced as the year ends.

The performance figures presented represent a total inventory methodology which assumes all hotel rooms are available with the exception of hotels closed for more than six months or those that have changed use to things such as college and university dorms. For this reason, it is important to note the dramatic changes to supply which have taken place as a result of the ongoing pandemic.

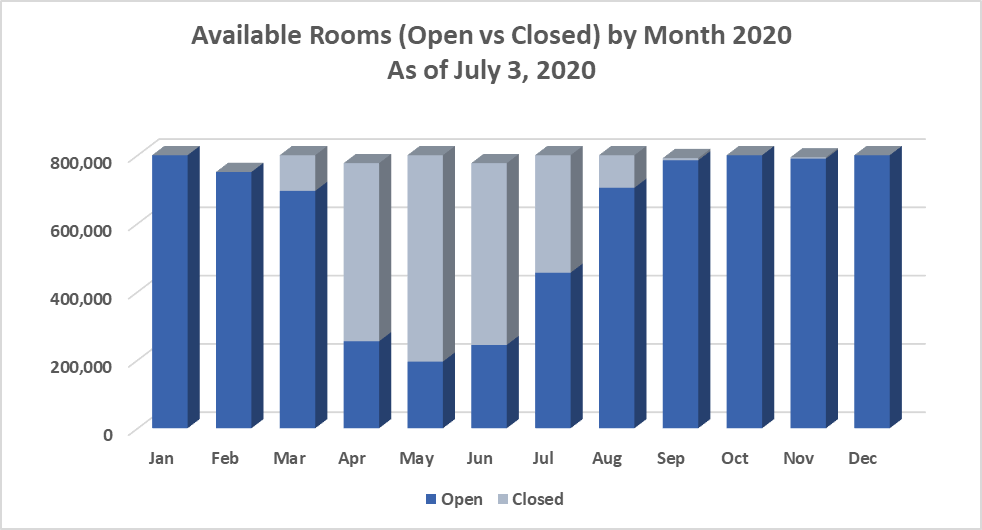

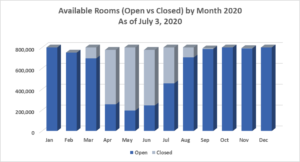

The majority of hotels in Boston and Cambridge closed in late March or early April and some are still closed through the end of September with no plans in place to reopen. Hotels were given the green light to open as part of the State’s phased reopening process on June 8.. Given the low levels of demand, the unclear guidance on reopening and accepting of out-of-state travelers, many owners and operators took a more cautious approach choosing to open much later. Based on information provided to Pinnacle Advisory Group from individual hotel owners and operators as well as the Greater Boston Convention & Visitors Bureau, we estimated the number of available rooms which ultimately closed. Available rooms supply in March was reduced by approximately 15% of its actual amount. This increased to almost 70% in April and reached a peak of 78% in May. Hotels were permitted to reopen in June however the market’s supply increased to only 30% of its actual size. A considerable number of hotels opened in July and August as available rooms increased to 50% and 70% of its actual inventory, respectively. In September, approximately 15% of the market’s hotel supply was still closed or operating as a different use (ie. dormitory for local universities and colleges) and we believe supply will remain at a similar level until Q1 2021.

Pinnacle Advisory Group presented its projections (found here) for the Boston & Cambridge and the Boston suburbs in August as part of Massachusetts Lodging Association’s Annual Outlook event. Given the frequent changes facing the industry, Pinnacle will update these projections at the end of October and update quarterly moving forward.

About Sebastian Colella:

Sebastian J. Colella is a Vice President with Pinnacle Advisory Group based in the Boston office. With over 15 years in the hospitality industry, Mr. Colella leverages his operational knowledge and expertise from experiences in the field. Work with Pinnacle Advisory Group has included market and feasibility analysis, acquisition due diligence, departmental revenue and expense performance evaluations, facility recommendations, brand assessments and impact studies, as well as appraisals of both branded and independent hotels and resorts.

Prior to joining Pinnacle Advisory Group, Mr. Colella held a variety of management roles in hotels, resorts and private clubs. With capacities focusing on both sales and operations, he has worked for ClubCorp, the world leader in private clubs, Rosewood Hotels’ flagship property in New York City, The Carlyle, and led efforts to open the first luxury resort in Zanzibar, Tanzania, Baraza Resort & Spa. Sebastian is a graduate of the School of Hotel Administration at Cornell University and currently serves as the President of the New England Chapter of the Cornell Hotel Society.

September 9, 2020 2:08 pm

Comments Off on Rhode Island Hospitality Economic Outlook – by Rachel Roginsky, ISHC Click on the title below to view the presentation:

Rhode Island Hospitality Presentation 2020

August 20, 2020 9:42 pm

Comments Off on Outlook 2021 – Rachel Roginsky, ISHC Click on the title below to view or download the Outlook 2021 presentation given by Rachel Roginsky, ISHC, for the Mass Lodging Association:

Final – Outlook 2021

July 28, 2020 9:02 pm

Comments Off on Hotel Operators Cautiously Plan to Reopen in Boston & Cambridge Amid Coronavirus Concerns – by Rachel Roginsky, ISHC and Sebastian Colella During the early stages of the ongoing pandemic, the Boston & Cambridge lodging market was one of the most heavily hit markets in the country. As part of the state’s phased reopening process, hotels were allowed to reopen in June, however, it became clear that most hotels would take a more cautious approach to restarting operations. As of the first week of July some hotels have remained closed, others have opened with limited inventory, while others may face permanent closure. Additionally, the pipeline of proposed hotels for Boston and Cambridge has been disrupted due to construction delays, an eight-week moratorium on all construction in Boston and ten-week moratorium in Cambridge, lack of financing, and general uncertainty. COVID-19, the disease caused by the new coronavirus, has not only negatively impacted lodging demand for years to come but it has dramatically changed the local market’s rooms supply.

As the number of cases increased locally in early to mid-March, government officials declared a state of emergency, restricting travel and large gatherings. Many hotels in Boston and Cambridge began operating at single digit occupancies, forcing owners to close their hotels and layoff, furlough, or reduce hours of their workforce. The hotels which remained open during these months, many of which are in close proximity to the city’s major hospitals, remained open to accommodate patients, first responders, and other contract demand.

As of March 1, 2020, the Boston & Cambridge lodging market was made up of 114 hotels with over 25,900 rooms. Based on information provided to Pinnacle Advisory Group from individual hotel owners and operators as well as the Greater Boston Convention & Visitors Bureau, we know that many hotels closed the last week of March. As a result of these closures, we have estimated that available rooms supply in March was reduced by approximately 15% of its actual amount. In April, 65% of the market’s rooms were offline and in May the number of closed rooms increased further to above 75%. Although hotels were permitted to reopen June 8th, only a select few hotels reopened in the month, increasing the market’s supply to only 30% of its actual size. Operators are optimistic that pent up leisure demand and the market’s ability to capture the regional travelers from the northeast will help to increase lodging demand in the summer and fall months. For this reason, a considerable number of hotels have plans to reopen in July and August. Based on the planned reopening dates provided to Pinnacle Advisory Group, approximately 60% of the market’s rooms supply will be open in July and will then increase to approximately 85% in August. Outside of the properties which may be closed permanently, we expect most hotels to be open by September however we understand that there is a considerable amount of uncertainty in today’s market as it relates to the spread and threat of COVID-19 and reopening plans will likely change.

click on image to enlarge:

Source: Pinnacle Advisory Group, Greater Boston Convention & Visitors Bureau

Estimated openings as of July 3, 2020, subject to change.

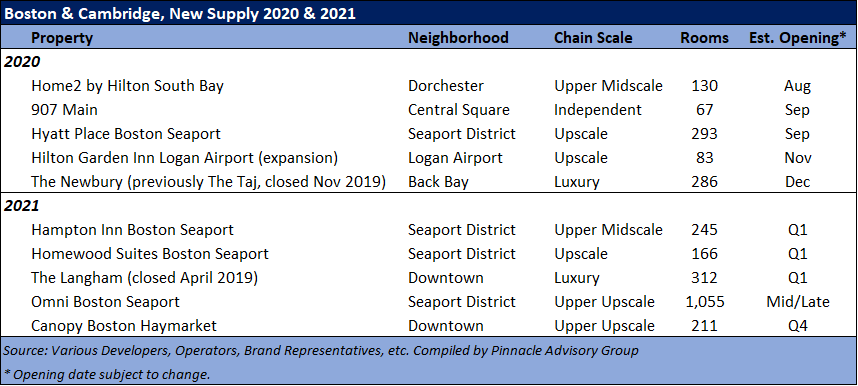

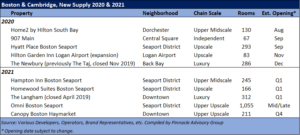

Pinnacle Advisory Group reported on the new hotels opening in 2020 and 2021 in January of this year and had forecasted rooms supply in Boston & Cambridge to increase 3.8% in 2020, well above its long-term average annual growth rate of 2.4%. Six hotels with almost 1,000 new rooms were expected to open throughout 2020. Additionally, there was a considerable number of rooms which came online in Q3 and Q4 of 2019 and both The Langham and The Taj (now The Newbury) were expected to reopen in the second half of 2020. The forecasted increase to the market’s rooms was to represent the second year in a row with supply growth of over 3% and the second highest increase in rooms supply since The Great Recession in 2008/2009.

Based on conversations with hotel developers, brands, and operators with projects underway in Boston and Cambridge, the hotels which were under construction in March of 2020 will be delayed to varying degrees. Those which were in the final stages of construction and near completion are expected to be delayed two to four months. Hotel projects that were in earlier stages with openings later next year could face longer delays depending on the size of the project. When accounting for the delayed openings and the temporary closures that began in March, rooms supply is now expected to increase 1.8% in 2020.

The new hotels entering the market in 2020 and 2021 are outlined below. There are hotels under construction with opening dates in 2022, such as the 147-room Raffles Boston Back Bay, and others which are in early and late planning stages and likely to open in two to four years.

click on image to enlarge:

Owners and operators in the Boston & Cambridge lodging market enjoyed considerable growth in revenue over the last ten years, however that growth began to slow in 2017 as market fundamentals began to shift. The impact from the ongoing pandemic hit the market in mid to late March and has since devastated its performance and disrupted its supply. As owners and operators prepare for changes to their day-to-day operations, many of which will increase operating costs, we do not believe that market fundamentals, a combination of demand and room rates, are unlikely to return to previous levels for three to five years.

Rachel Roginsky, ISHC is the Founder and Principal of Pinnacle Advisory Group. She is based in the firm’s Boston office. Ms. Roginsky has more than 35 years of experience in hospitality consulting.

Sebastian J. Colella is a Vice President with Pinnacle Advisory Group based in the Boston office. Sebastian has over 15 years of experience in the hospitality industry.

July 16, 2020 11:21 am

Comments Off on How Much Is A Hotel Worth? – by Allison Fogarty In the case of property tax assessments in Florida, probably somewhat less than the county property appraiser assumes. A recent court decision invalidated the method used by many county property tax appraisers in Florida to develop “just” values for hotels.

The Background

Walt Disney Parks and Resorts successfully argued that the Orange County Property Appraiser improperly considered income from the business activities conducted on the premises in establishing the just value of the Disney Yacht & Beach Club Resort which includes restaurants, retail shops, a spa and convention center in addition to its 1,197 guest rooms.

Florida’s Constitution requires annual reassessment to determine the “just” or fair market value of the “Real property” defined as land, buildings, fixtures, and all other improvements to land. Notably, real property specifically does not include personal property and “Intangible personal property” which includes all other forms of property where value is based upon that which the property represents rather than its own intrinsic value.[1] The Orange County Property Appraiser’s staff, in common with most county appraisers, considers eight statutory factors in deriving just value, but places greatest reliance on the Income Approach. Resources available to county appraisers include access to sales tax returns. The Orange County Property Appraiser (Appraiser) also sends an annual income and expense survey to each of the county’s numerous hotel properties.

Hotels are complex assets, combing real estate with an operating business that takes considerable marketing, management, and financial skill to operate successfully. In addition, an operating hotel includes a significant investment in personal property – the furniture, fixtures, and equipment, which incudes everything from beds, to stoves, to computers. In general, when hotel properties are purchased as a going concern, investors /purchasers are focused on the overall EBITDA projected for the asset, any capital improvements necessary to achieve that EBITDA, their risk assessments and ROI requirements. Most hotel investors do not allocate yield between realty and non-realty components of the business in making their investment decisions, and most hotel mortgages are package loans which include the FF&E. Allocating the value among the various components is however critical in determining ad valorum taxes, which include real estate taxes, sales tax (on transfers of personal property included in a transaction) and documentary stamp taxes on transfers of real estate.

The Orange County Tax Appraiser used a methodology popularized by Steve Rushmore to remove the income attributed to the business and personal property components from the hotel’s overall value. Briefly, the value associated with the management is deducted via a management fee, the value of a brand is attributed to the franchise fees and the value of the FF&E is deducted from the overall capitalized net income. [2] Disney argued that this approach, adopted by the county appraiser, underestimated the intangible assets associated with the property including the value of the brand/copyright/ goodwill, loyal customers, and an assembled workforce.

The Court’s Analysis and Conclusions

The original trial court found that the Appraiser improperly considered income from business activities conducted on the property in establishing the just value of the property, and rejected the Appraiser’s contention that the intangible assets identified by Disney did not qualify as intangible property. [3] The appeal court found that the Appraiser’s methodology inappropriately included the value of Disney’s intangible business assets in developing its assessment, because it did not provide for adjustments to the gross business income for intangible business value prior to deducting franchise and management fees. The court concluded that “the Rushmore Method ignores the fact that an intangible business value may be directly benefiting a business’s income stream”[4] and found the “explanation of how the deductions for franchise and management fee expenses removed the entire intangible business value from Disney’s income stream is unconvincing”[5]. The Florida Court also noted that a California court had similarly found that an assessment determined by the Rushmore Method had failed to exclude intangible assets in contravention of California law.( SHC Half Moon Bay v. County of San Mateo, 171 Cal. Rptr. 3d 893, 911) (Ct. App. 2014). The Florida Appeals Court also agreed that the space used to generate ancillary income – that is income from sales of food, beverage, retail merchandise and other services (such as the spa) – should be valued differently from the rooms operation. Although it disagreed with some technical aspects of Disney’s capitalization of the comparable rental value of the restaurant, retail, and spa spaces, it seemed to agree that Disney’s methodology was reasonable.[6] Ultimately, the Appeal Court has determined that the Property should be reassessed using a methodology consistent with the its opinion.

Implications

Since many of the county appraisers throughout Florida use the “Rushmore Method” to assess hotel properties, this decision has wide ranging implications for hotel properties in Florida, particularly full service properties and larger resorts, where rooms revenues represent a smaller percentage of the property’s total revenues. The value of some comp services (airport shuttles, concierge services, free parking, luggage handling) offered to guests may be deductible in determining the ADR associated with the real property component of the operation. It is evident, at least in Florida and California, that taxable real estate values heavily reliant upon the Rushmore Method are vulnerable to appeal.

This ruling may also imply that properties that achieve above average results, though a combination of branding, management and service have some justification or arguing that they should not be penalized with higher property taxes for their superior operating performance.

Clearly intangible business value my be in for closer scrutiny in the lodging industry over the next several years.

[1] Chapter 199 Florida statutes

[2] Rushmore, Stephen. In Defense of the “Rushmore Approach” for Valuing the Real Property Component of a Hotel”.

[3] Rick Singh, as Property Appraiser v. Walt Disney Parks and Resorts US, (Fla. 5th Dist. Ct. App. 2020) Pg. 8

[4] Ibid Pg. 11

[5] Ibid, pg. 12

[6] Ibid. 13 -16

About Pinnacle Advisory Group

Since 1991, Pinnacle Advisory Group has provided advice and analysis on the full spectrum of hospitality properties throughout the US and Caribbean: hotels, resorts, conference centers, mixed use projects, convention centers and exhibition centers. Pinnacle’s services include development counseling, appraisals, acquisition due diligence, asset management and litigation support. Our clients include leading hotel companies, REITs, universities, major banks, and municipalities. We conduct appraisals for portfolio review, litigation, loans and property tax purposes. We specialize in providing personalized advice on complex projects, carefully tailoring our services to each client’s individualized needs.

About the Author

Allison Fogarty is the Managing Director of Pinnacle Advisory Group’s Florida and Caribbean Practice Group. Ms. Fogarty has extensive experience in hotel and resort financial analysis and development. Her activities have included site selection, property inspection, contract negotiation and review and due diligence. As a consultant, she has directed and completed market and financial analysis engagements and investment counseling for hotels and resorts in the eastern United States and the Caribbean.

July 14, 2020 7:50 pm

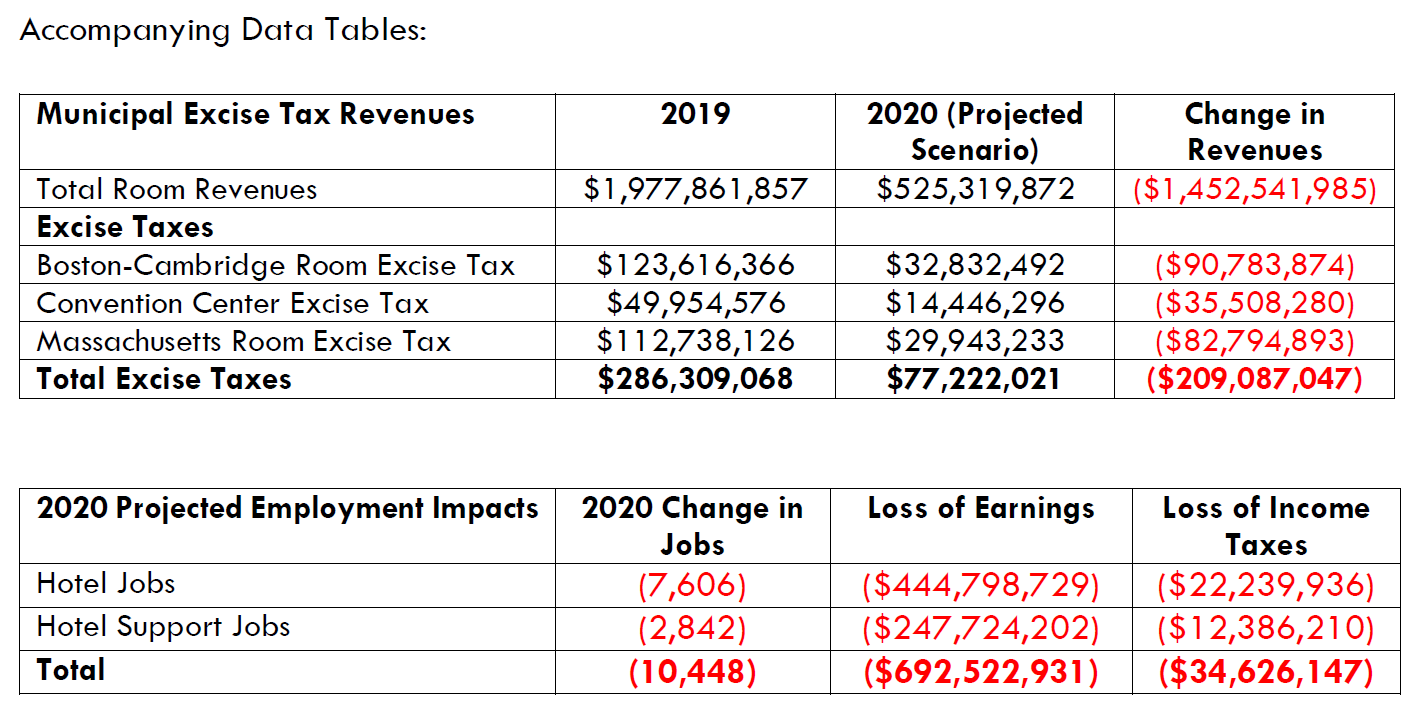

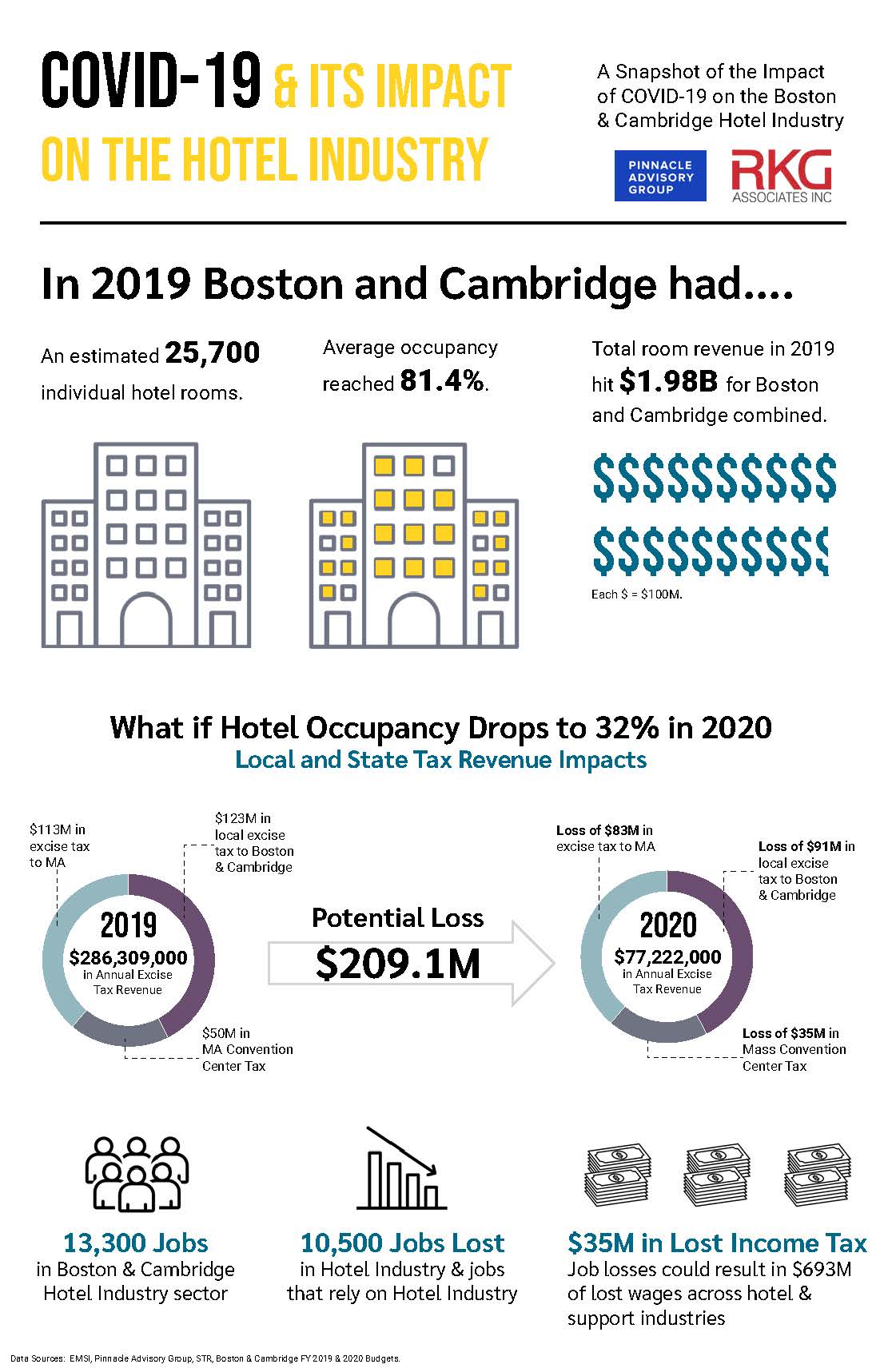

Comments Off on Impacts of COVID-19 on the Boston and Cambridge Hotel Industry – by RKG Associates and Pinnacle Advisory Group For 2019, Pinnacle Advisory Group estimated that Boston and Cambridge hotels generated nearly $2 billion in rooms revenue, based on a total supply of nearly 25,700 rooms, an average occupancy of 81.4 percent and an average daily rate (ADR) of $259. Over 13,300 people are employed in the hotel industry sector in Boston and Cambridge. Due to the pandemic and the stay-at-home requirements starting in March of this year, demand for hotel rooms has dropped precipitously. On March 31, Governor Baker began a provision of lodging that was defined as a COVID-19 Essential Service, allowing hotels in the state to service only essential workers and other people with essential status. Occupancy of lodging for leisure, vacation, and other purposes was halted. On June 8, Phase 2 began, allowing hotels to reopen with certain limitations.

According to the Pinnacle Perspective, Revenue Per Available Room (RevPar) declined 98% for May 2020 as compared to the prior year. Hotel occupancy for May 2020 dropped to 6%, and when compared to May 2019 is a decrease of 94%. Hotels in the Back Bay recorded the lowest average occupancy in the Boston/Cambridge market at 1.5% for May 2020. We anticipate hotel occupancy and RevPar to begin increasing in June and July as the Commonwealth continues its phased re-opening plan. While most conferences and events will be extremely limited; offices and work-related travel and leisure visitation are likely to slowly increase.

To estimate the economic impacts, Pinnacle and RKG Associates assumed a worst-case scenario where the annual occupancy rate for 2020 drops to 32 percent and the average daily rate to $175. This assumes that the economy begins to recover in late summer and early fall but does not regain its former strength, including a severe cutback in tourism, conventions, and international visitation – a mainstay of the city’s hotel industry. These impacts were analyzed using EMSI, a leading econometric modeling tool, to determine the direct, indirect, and induced impacts on the two cities and the region’s economy.

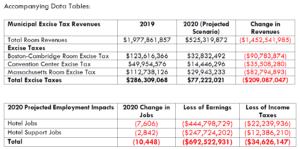

Under this scenario, hotel revenues decline by over $1.4 billion and 7,606 hotel jobs would be negatively impacted. Additionally, we estimate another 2,842 jobs in industries that support the hotel sector would also be impacted, resulting in a total of $693 million in lost wages. This in turn would result in a loss of over $34 million in state income taxes. Massachusetts room excise taxes would decline by $83 million, while Boston and Cambridge would lose nearly $90 million in local option rooms tax. The rooms tax comprises 2.8% of Boston’s annual budget and 2.3% of Cambridge, a shortfall that will need to be made up somewhere else. The Convention Center tax, of 2.75% of room sales, goes to support the Massachusetts Convention Center Authority. This loss is estimated to be just over $35 million.

While a 73 percent drop in RevPar over last year may seem extreme, it is not out of the question, given the length of time it is taking to get the economy back on track, and the long-term impacts the pandemic will have on business activity and tourism.

Click on image below to view accompanying data tables:

Click on image below to view infographic:

Working closely with Pinnacle Advisory Group LLC, a leading hospitality industry consulting firm, RKG Associates analyzed the potential impacts of the current pandemic on the hotel industry in Boston and Cambridge.

Craig Seymour and Eric Halvorsen, AICP are Principals with RKG Associates. RKG is an economic, planning, and real estate consultancy with offices in Washington, DC, Boston, Atlanta, Dallas, and Durham, NH. Since its founding in 1981, RKG has built a track record of sound planning advice rooted in data, creativity, and realistic, implementable strategies. RKG’s strength is in a diverse range of experiences that have helped hundreds of cities, towns and private firms make the most of spaces that matter to them. RKG specializes in economic analyses, market studies, financial forecasting, strategic planning, feasibility analyses, real property valuations, and housing strategies. www.rkgassociates.com

Rachel Roginsky, ISHC, is the Owner and Principal of Pinnacle Advisory Group. Ms. Roginsky has more than 35 years of experience in hospitality consulting. Since 1991, Pinnacle Advisory Group has provided advice and analysis on the full spectrum of hospitality properties throughout the US and Caribbean: hotels, resorts, conference centers, mixed use projects, convention centers and exhibition centers. Pinnacle’s services include development counseling, appraisals, acquisition due diligence, asset management, workouts, and litigation support. Our clients include leading lenders/investors, hotel companies, universities, and municipalities. We specialize in providing personalized advice on complex projects, carefully tailoring our services to each client’s individualized needs. www.pinnacle-advisory.com

May 19, 2020 1:21 pm

Comments Off on Pinnacle Advisory Group and Boston University – New England Lodging Conference Takeaways THE NUMBERS: DATA, FACTS & FORECASTS. With Rachel Roginsky, ISHC, Jim Berry (Cushman & Wakefield), and Mark Woodworth (R.M. Woodworth & Associates).

Brought to you by Pinnacle Advisory Group and the Boston University School of Hospitality Administration. This event connected leaders in the lodging sector to share insights and today’s take on occupancies, rates, RevPAR, legal issues, and operational challenges for the hotel industry in the region.

Click below to view the presentation slides:

New England Lodging Conference Presentation

1:14 pm

Comments Off on Hotels at Secondary and Tertiary Airports Will Suffer Longer – by Jenny Lee The coronavirus pandemic’s impact on travel is thought to be six or seven times greater than the 9/11 attacks, according to the U.S. Travel Association. Air travel volume fell precipitously through March. The estimated revenue losses by air carriers in 2020 is at least $252 billion. In late March, domestic carriers received a $60 billion bail-out, with some strings attached.

The Department of Transportation issued an order that carriers receiving financial assistance under the Coronavirus Aid, Recovery, and Economic Security Act (the CARES Act) are required to maintain minimum air service to all destinations served as of the last week of February (with some exceptions).

The Show Cause Order stated that in cases where multiple airports serve the same point, covered carriers would not need to maintain service to all airports but would be able to consolidate operations at a single airport serving the point. Due to this caveat, we believe that airport hotels at secondary and tertiary markets will have their occupancies severely impacted and will be among the last to come back.

For example, with flight consolidations at Los Angeles International Airport (LAX), the Burbank, Long Beach and Ontario airports will probably suffer. The same is predicted for San Jose and Oakland airports after consolidating at San Francisco International Airport (SFO). Other secondary and tertiary airports likely to be affected include Dallas’ Love Field and Chicago-Midway, among others.

The definition of “same destination” is being stretched. Despite taking the bail-out:

- Delta has asked to suspend service in Melbourne FL; Brunswick GA; Pocatello ID; Worcester MA; Flint, Kalamazoo and Lansing MI; and Hilton Head, SC;

- United had earlier tried, unsuccessfully to suspend service to Kalamazoo MI, Santa Fe NM and Green Bay Wisconsin.

Frontier, Jet Blue, and Spirit, which are under a slightly different set of rules, are asking for waivers for bigger cuts:

- On April 27, Frontier received waivers for suspending service to Detroit, Charlotte and the Boston area. Frontier had originally asked approval to suspend service to 33 U.S. airports through June 10, but only three locations were granted.

- JetBlue has asked to halt flights to 16 U.S. airports, including Chicago, Atlanta, Houston, Seattle, Las Vegas, Philadelphia, Dallas and Detroit through September 30.

- Spirit has asked for approval to suspend flights to Charlotte, North Carolina, Denver, Minneapolis/St. Paul, Seattle, Portland and Phoenix.

It is uncertain at this time how many waivers the Department of Transportation will issue but as more markets consolidate, the hotels in secondary and tertiary markets will surely be impacted.

The Service Obligation pertains to only U.S. destinations and is scheduled to extend through September 30, 2020, the same date under the CARES Act through which carriers must maintain certain levels of employment. This date may be extended to a later time, for all or portions of covered carriers and covered points.

The latest surveys indicate that air travel, in particular, will be challenged. In recent research for the U.S. Travel Association, 67% of respondents indicated they would take a trip by car in the next 6 months, but only 32% said they would take a domestic flight within that window. International travel was even lower, at only 19% of the respondents planning an international flight within the next 6 months.

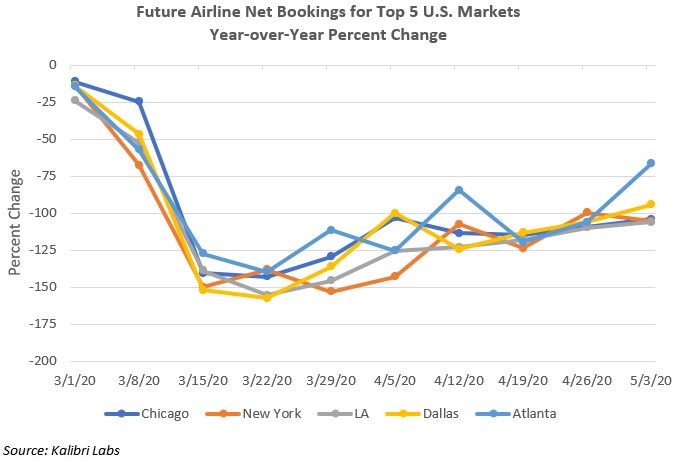

Future airline net bookings dropped significantly in the nation over the past few months. According to Kalibri Labs and Forward Keys, airline net bookings through December 2020 in the U.S. hit a low of negative 173.0% for the week of March 16 to March 22 compared to same period last year. The outlook is still grim with negative 107.8% net bookings for the week of April 27 to May 3. Week-over-week overview of net booking trends (including cancellations) for major U.S. destinations through December 2020 is shown below:

Click on image to enlarge.

Most analysts believe that the industry will recover by the year 2022, at the latest. But until vaccines and drug treatments are developed, airport hotels, especially those located in the secondary and tertiary markets, will be on a long road to recovery and among the last to recover.

May 15, 2020 8:52 pm

Comments Off on Lack of Clear Travel Guidelines Leaves New England Lodging Market in Limbo – by By Rachel Roginsky, ISHC and Sebastian Colella Hotels throughout New England are normally preparing for their peak season this time of year. Unfortunately, 2020 has been anything but normal. The impact of COVID-19 and the changes to normal day-to-day life have had severe impacts on lodging markets across the country. Many hotels throughout New England have temporarily closed and those that are open are limited to accommodating healthcare workers, other essential workers, the homeless, and those who are self-quarantining. As states roll out phased reopening plans, many hotel owners and operators in New England are now wondering what to expect for their summer and fall seasons, typically their busiest time of the year.

In 2019 the U.S. lodging market experienced a 2.0% increase in demand, accommodating an historic high number of roomnights, and achieving RevPAR (revenue per available room) of $85.96, its highest in history. While the year was off to a great start with RevPAR increasing 4.4% and 3.8% in January and February, respectively, the impact from coronavirus began to take its toll in March. Demand declined over 40% driving RevPAR down 52% when compared to the same time last year. The market segment that declined first, and with such magnitude, was the group segment. As such, many luxury and upper upscale hotels, the full-service hotels which rely on this segment most, experienced declines in occupancy. Since group demand is booked years in advance and typically at lower rates, average daily rates (ADR) was not as impacted in the short-term. As transient demand, normally the higher rated segment, began to decline, occupancy declined at a rapid pace, negatively impacting both occupancy and ADR as can be seen in the April data. Further, given the global nature of the pandemic, travel was being restricted from international destinations, which caused additional downward pressure to gateway market’s which have historically relied more on this demographic.

The tourism industry is a significant economic driver in each of the New England states, supporting hundreds of thousands of jobs and generating billions of dollars annually in each. New England’s peak season, running from June to October, is fueled by leisure and group travel with occupancies above 70% each month. In 2019, these five months made up almost 60% of the year’s total room revenue. The majority of visitors in the summer and fall months are motorists from the northeast US and Canada, typically comprised of couples and families. Group related travel during these peak months include tour groups, and regional corporations or associations that have meetings, as well as social groups attracted to the region’s beautiful settings.

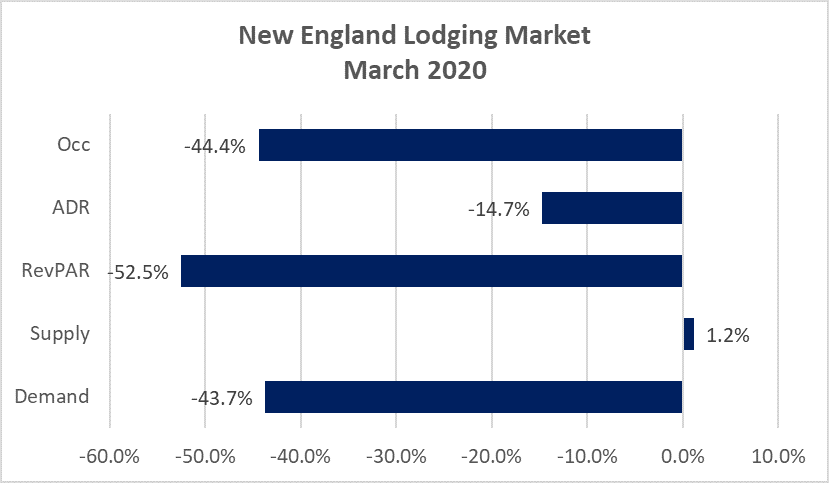

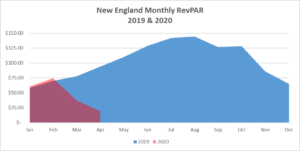

Similar to the trends in the US, the New England regional lodging market has been impacted by Covid 19. As can be seen in the following table, the declines in occupancy and ADR experienced throughout New England in March when compared to last year resulted in a revenue per available room (RevPAR) declined of over 52%.

click on image to enlarge: Source STR

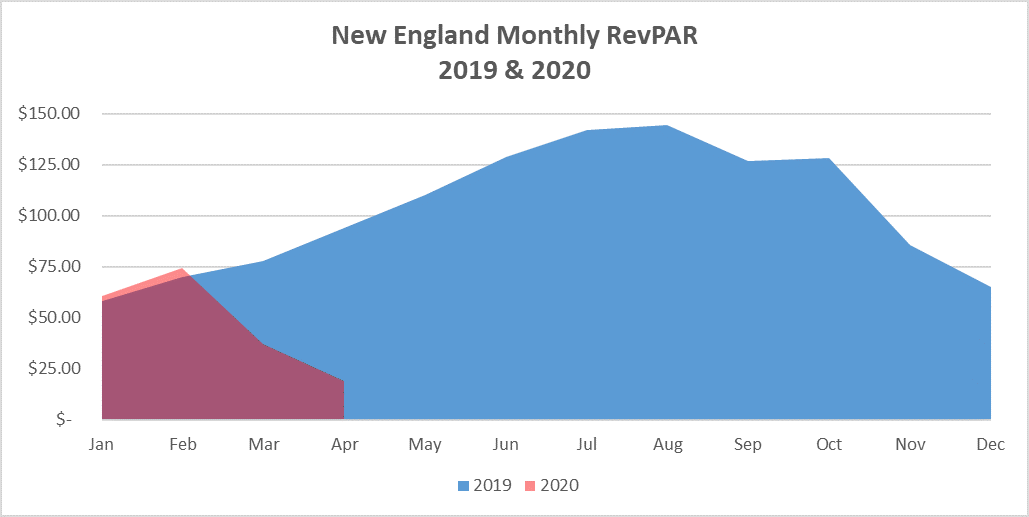

Although April figures for New England are not yet available, RevPAR is expected to decline between 75% and 85%. Preliminary results for the U.S. indicate a decline in RevPAR of approximately 80% in the month of April when compared to the same time last year.

click on image to enlarge: Source STR (historic performance), Pinnacle Advisory Group (projected April 2020 performance)

Although a recovery is likely to be slow and achieving 2019 performance levels could take years, destinations in the New England region could begin to see a pick-up in demand later this summer, potentially more so than other areas of the country. As states begin to loosen their travel restrictions many people will want to venture out after isolating for months. This pent-up demand will likely be focused on regional, drive-to destinations such as those throughout New England. Additionally, outdoor areas and attractions where visitors can distance themselves from others such as national parks and beaches will give visitors a sense of added comfort. Although unemployment is at its highest levels since the Great Depression, heavily discounted nightly rates and low gas prices will further encourage leisure travelers to plan vacations.

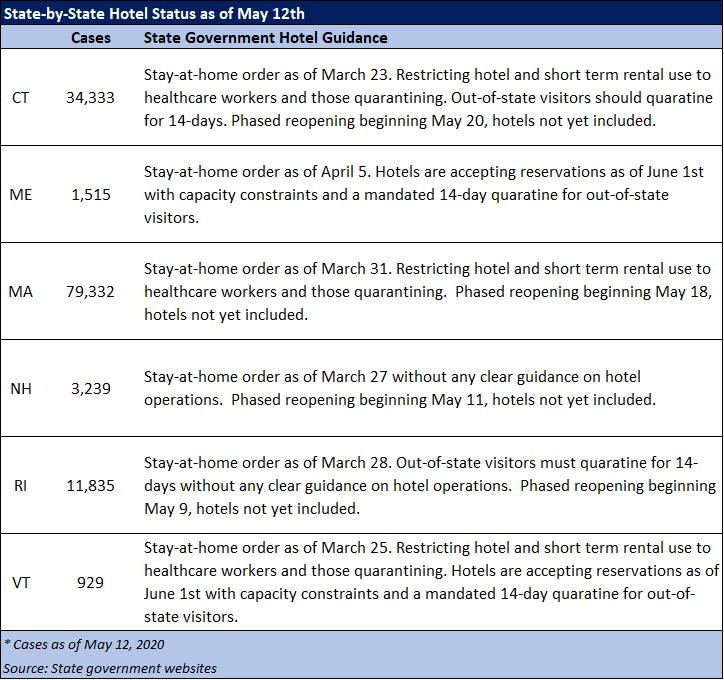

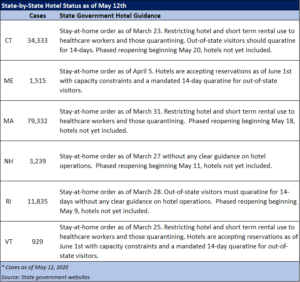

While this bodes well for New England tourism, lodging demand will not return without an easing of social distancing and travel restrictions combined with improved consumer confidence. State governments are facing difficult decisions to reopen businesses in order to lessen the economic toll of the coronavirus while also trying to limit health risks to their residents and visitors. Even as stay-at-home orders are lifted in some states, it is unclear how much longer COVID-19 cases will continue to rise or how successful the government’s response will be in mitigating its impact to individuals and the economy. Making things more confusing for both business owners and consumers are the different guidelines and mandates to commercial lodging businesses across all six states.

click on image to enlarge:

Owners and operators have endured massive losses since mid-March and are growing frustrated without clear guidance on when they can begin accepting reservations for out-of-state travelers without a mandated quarantine. Owners of seasonal hotels which open for four or five months a year are at risk of defaulting on their mortgages and could face bankruptcy. Although the year as a whole will not compare to the performance in 2019, operators are hopeful that bringing back leisure travel July through October will help mitigate the damage.

The leisure demand segment is expected to rebound first providing travel is allowed to return this summer or fall. But for that to happen consumers must feel a level of safety and they will need the financial means to do so. The manner in which each state reopens and welcomes out-of-state travelers will have a direct impact to the wellbeing of the regional lodging market.

About our Authors:

Rachel Roginsky, ISHC is the Founder and Principal of Pinnacle Advisory Group. She is based in the firm’s Boston office. Ms. Roginsky has more than 35 years of experience in hospitality consulting.

Sebastian J. Colella is a Vice President with Pinnacle Advisory Group based in the Boston office. Sebastian has over 15 years of experience in the hospitality industry.

April 29, 2020 6:34 pm

Comments Off on When to Reopen Your Hotel: The Decision to Shut Down was Hard but the Decision to Re-Open is even Harder – by Matthew R. Arrants, ISHC, CHAM Politicians and industry leaders are struggling with when to allow hotels to open. Even when policy changes, just because hotels can reopen does not mean they should. When the pandemic hit U.S. shores, owners and operators were immediately concerned with the health and safety of their employees and guests. As occupancy levels plummeted, owners and operators scrambled to determine at what level it was more “profitable” to stay open than to close. A common range was between 8% and 12% occupancy. With that analysis, they then considered things like the duration of the lack of demand. At that point in time, hotel owners had the clarity of knowing that things were going to get worse: cases would rise, and travel would be discouraged, if not banned, by the government.

Now, more than a month later, things appear to be getting better. Cases are leveling off in some places, and governments are looking at when and how businesses can reopen. The challenge for owners is balancing the desire to resume business as soon as possible and the reality that sooner isn’t always better, particularly when dealing with a pandemic recovery. When weighing the decision of when to reopen, owners should consider the following:

- Employee Safety – Employee safety always should be paramount. The industry is working diligently to develop employee protection protocols, but lack of consistency between local governments suggests that hotel owners must develop their own criteria, such as number of regional cases and available medical resources should an employee become ill.

- Guest Safety – If employees can safely work, the next consideration becomes the ability to keep guests safe. Owners and managers have to consider how on-going operations must be revised, from instituting remote check in and erecting plexiglass barriers at points of contact to opening food and beverage outlets on a to-go basis only.

- Employee Retention – Most employees have been furloughed and are technically no longer employees. Hotels that open too late risk losing those employees to competitors or other industries. The result could be increased training costs and reduced efficiency.

- Employee Recruitment – Seasonal markets may experience a shortage of skilled labor this summer. Factors expected to impact available labor include a lack of international labor, limitations on dormitory style employee housing and generous unemployment benefits that are paying more than individuals can earn at work. Properties that open too late could face challenges in meeting their staffing needs.

- Reputation – Hotels that stayed open or those that re-open early may benefit in the eyes of customers because they’ve demonstrated a commitment to their guests and their employees. They also run the risk of being thought of as a higher risk option, especially if it becomes public knowledge that a hotel employee or guest contract the virus.

- Profitability – Effective safety protocols likely will impact profitability. In general, larger groups are more profitable due to the efficiencies that they provide. In this new era of social distancing, group sizes will be limited, so efficiencies of scale (and therefore profitability) will be reduced. In addition to lost efficiencies, direct costs are likely to increase with more frequent cleaning and sanitizing. Lastly, there is a possibility that public policy will require guest rooms to sit empty for certain periods of time and/or that hotel occupancy levels will be limited to reduce guest interaction in corridors, public space and elevators.

- PPP Loans – Many owners applied for and received loans through the Paycheck Protection Plan included in the Care Act. For portions of loans to be forgiven, employers must meet certain requirements that include putting employees back on payroll within a certain period of time of receipt of the loan.

- Demand – Perhaps the most challenging factor facing owners is forecasting demand. Many experts predict that leisure will be the first segment to return, followed by corporate and ultimately group demand. Within those segments, drive-to destinations will come back before destinations that rely heavily on airlift, such as gateway cities and islands. While these considerations provide some framework for the timing of demand, they don’t give an indication of how strong demand will be. Many guests likely will base their decision to travel on government issued guidance, which in turn will be based on the ability to test and track outbreaks. At this point, there appears to be little certainty as to when effective testing and tracking will be available. Lastly, the unstable economy compounds the challenges of projecting demand. Many consider the current situation to be far worse than the great recession of ten years ago.

The considerations outlined here are general ones that all owners face. There are more that are specific to each property. In addition, each of these considerations apply differently to every hotel. While there is no perfect re-opening date for any one property, owners will be well served by carefully weighing all the above considerations in light of the facts on the ground.