Author Archives: Amanda Wiggins

April 28, 2021 1:35 pm

Comments Off on Update to the Massachusetts Lodging Association’s Annual Outlook Projections – by Sebastian Colella Pinnacle was pleased to prepare an update to the Massachusetts Lodging Association’s Annual Outlook projections. The updated presentation provided actual performance through Q1 for the State, the Boston MSA, and the Boston & Cambridge Lodging markets. Looking ahead, Pinnacle outlined key factors which indicate a recovery will begin to take shape in Q2 of this year. While there are still many unknowns for the remainder of 2021, Pinnacle’s yearend projections for Boston & Cambridge point to accelerated demand growth in Q3 and Q4. The overall Boston market has been one of the most severely impacted markets in the country. As a result of this and other factors, the market is expected to have a longer recovery period than many other major markets.

Click on images below to enlarge:

Click on the link below to view the entire presentation:

MLA Outlook Q2 2021

1:22 pm

Comments Off on CHMWarnick and Pinnacle Advisory Group Form Strategic Alliance Move Collectively Broadens Service Offerings to Provide Additional Asset Management and Advisory Services to Current and Future Clients

BOSTON, April 28, 2021—Officials of CHMWarnick, the leading hotel asset management and owner advisory services company, and Pinnacle Advisory Group, a premier national hospitality consulting firm and women-owned business, today announced the formation of a strategic alliance. CHMWarnick and Pinnacle boast company track records spanning 25 and 30 years, respectively. The move leverages vast industry experience and reputation, while broadening the business platform, depth of expertise and knowledge base of both companies to provide superior asset management and hospitality advisory services to their respective clientele.

“The new pandemic reality has resulted in a tremendous surge for assistance from an increasingly larger pool of hotel owners, investment groups and lenders,” said Chad Crandell, managing director and CEO, CHMWarnick. “Whether it is advice on how to deal with an existing hotel in an underperforming market, assessing acquisition or development opportunities or simply strategizing logical next steps, hoteliers need experienced, financially prudent guidance. This alliance strengthens both companies’ abilities to respond to an ever-changing landscape as the hospitality and travel industries continue to rebound from the COVID-19 pandemic, as well as support clients looking to take advantage of investment opportunities that this unique period presents.”

Combined, the strategic alliance immediately will service an asset management portfolio approximating 80 hotels with more than 32,000 rooms nationwide, representing virtually all segments and major brands, including among others, Marriott, Hilton, Hyatt, IHG and Accor, as well as a growing number of high-profile independent and lifestyle properties and select-service portfolios. The entities specialize in convention headquarter hotels, complex resorts, urban lifestyle and luxury properties, upper-upscale landmark assets, select-service and extended-stay hotels, as well as properties proximate to airports and college and university campuses. Beyond the $15 billion in lodging real estate overseen as part of the asset management platform, the alliance collectively is advising owners and lenders on approximately 250 lodging projects annually, including hotel development, repositioning, management/brand selection, operations assessment, acquisition due diligence and ownership-entity accounting services.

Pinnacle has guided clients on a wide range of critical decisions throughout the life of a hotel investment, from initial feasibility and branding strategy to operational reviews and competitive impact studies. Often, Pinnacle’s work is on the front end of an investment strategy, providing due diligence and advisory prior to the development of an asset or during the initial stage of an acquisition. The alliance provides an opportunity for Pinnacle clients who may be looking to continue with professional oversight to access CHMWarnick’s asset management and accounting platform and related services geared toward value enhancement. Likewise, CHMWarnick can tap into Pinnacle’s market research, trends analysis and related expertise to support their clients with acquisition opportunities, strategic repositioning and development planning and on asset management engagements.

The affiliation will bring a combined professional staff of more than 50 industry experts across 13 offices nationwide.

“We saw this as an ideal match between the two companies – we fit like a hand in a glove,” said Rachel Roginsky, principal, Pinnacle Advisory Group. “Both of our groups are recognized as leaders within the industry with reputations for delivering sound, strategic advice based on decades of experience. By drawing on each company’s distinct strengths, this alliance allows us to offer the most comprehensive services available and expanded benefits for our clients.

“Furthermore, we’ve had multiple occasions where we’ve worked together throughout our respective histories, from joint membership and presently holding multiple board positions with such prestigious organizations as the Hospitality Asset Managers Association (HAMA), the International Society of Hospitality Consultants (ISHC) and the Castell Project,” Roginsky added. “While we are formally announcing our alliance today, our groups actively have been working together in a collaborative capacity for several months, across multiple client engagements. The synergies between our groups have proven invaluable, and I’m looking forward to building upon our early success in delivering incremental value and benefit to our clients.

“We believe the need for asset management and advisory services only will increase as hoteliers seek the best solutions to protect and optimize their investments. There is no ‘one-solution-fits-all’ approach. Markets will respond at different times and in different ways. Institutional investment, big-box hotels have been hard hit particularly. Lenders are demanding loan payments now and strategic plans on how properties will emerge stronger and better positioned. The encouraging news is that with the continued vaccine roll-out and a seemingly reinvigorated approach to directly dealing with COVID-19, the light at the end of the tunnel finally is coming into clearer focus,” Roginsky stated.

Both CHMWarnick and Pinnacle Advisory Group pride themselves on their ability to pivot quickly to meet client demands. While the move automatically adds bench strength to each company, the companies stress that internal expansion is equally important to their long-term growth plans. “The key to longevity is adaptability,” Crandell noted. “We both believe in the importance of cultivating talent from within, particularly as the universe of service providers has exploded, with some being obviously more talented than others. The alliance further allows us to provide additional mentoring and growth paths for our team members looking to expand their own careers.”

About CHMWarnick

CHMWarnick is the leading provider of hotel asset management and advisory services on behalf of owners and lenders. The company asset manages over 70 hotels comprising approximately 29,000 rooms valued at roughly $15 billion and is advising on development projects valued at over $2 billion. CHMWarnick’s services include asset management, loan monitoring, hotel receivership, hotel planning and development, acquisition due diligence, owner-entity accounting, management/operator selection and negotiation, capital planning, and disposition. CHMWarnick is regarded as a thought leader in hotel ownership issues and asset management practices, and has six offices nationwide, including locations in Boston, New York, Los Angeles, Phoenix, Fort Lauderdale, and San Francisco. For more information, contact 978.522.7002 or visit www.CHMWarnick.com. For the latest company news, follow CHMWarnick on Twitter @CHMWarnick and LinkedIn.

About Pinnacle Advisory Group

Founded in 1991, Pinnacle Advisory Group is a premier, national hospitality consulting firm with significant experience with consulting services pertaining to hospitality facilities throughout the United States and the Caribbean.

Pinnacle provides consulting services to a wide range of clients, including the traditional players in the hospitality industry – investors, lenders, and operators as well as the country’s major real estate investment and development firms, pension funds, REITs, insurance companies. Pinnacle executives are frequently cited as industry experts and the fruits of our research and analyses are used at the highest levels in the hospitality industry for key decision-making purposes. Pinnacle possesses this level of expertise across the full spectrum of hospitality-related investments: hotels, resorts, conference centers, interval ownership resort facilities, golf courses, ski areas, marinas, and public assembly facilities, including theme parks, arenas, convention centers, and exhibition centers. Pinnacle Advisory Group is a SOWMBA – Woman Owned Business. For additional information, please visit https://pinnacle-advisory.com

April 27, 2021 5:38 pm

Comments Off on Article for HNN – Silicon Valley Hotel Outlook: Darkest Before the Dawn Reliance on Tech Industry Struck Market Hard in 2020 – by Karen Johnson, ISHC, & Lana Yoshii Tech companies were among the first employers to cancel meetings and halt travel as news of COVID-19 emerged from China.

After first restricting international travel in February, most companies had restricted nonessential domestic travel by early March. Amazon and Facebook were conducting job interviews by video calls, and Twitter issued work-from-home orders well before counties issued shelter-in-place orders on March 16.

How bad was it, on a macro level?

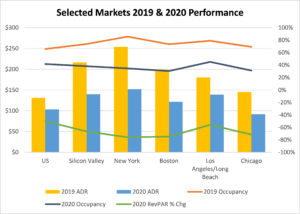

The U.S. hotel industry finished 2020 with a 50% decrease in revenue per available room versus 2019 results. While a 67% decline in Silicon Valley was significant, when stacked up against some U.S. hotel markets, Silicon Valley did not fare that badly. Hotel RevPAR in New York, Boston and Chicago declined between 72% and 76%. Despite the dive in occupancy, Silicon Valley “only” discounted rates by 35%, compared to 40% in New York, 39% in Boston, and 37% in Chicago.

click on image below to enlarge:

NOTE: Based on total rooms inventory: all temporarily closed hotel rooms supply calculated as if they were open.

Source: STR, compiled by Pinnacle Advisory Group, West.

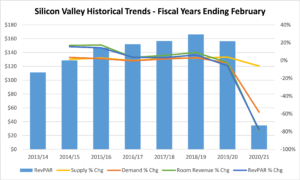

Looking at the trailing 12-month periods ending in February, Silicon Valley’s hotel market peaked with a 3% increase in demand, exceeding the 2.7% increase in supply, with an impressive 8.9% increase in room revenue, resulting in RevPAR of $166.27 at the peak. Though the market posted a 3.8% increase in hotel supply for the 12-month period, demand fell by 2.8%, resulting in a 5.9% decline in RevPAR for the core cities in Silicon Valley.

How to explain the pre-COVID-19 decline in demand, given that the tech industry was booming? The softening in demand started in April 2019 as price resistance accelerated. Travelers looked to lower cost markets in the East Bay area or made day trips.

With Silicon Valley hotels allowed to serve only essential workers, occupancy in the market dove to 16.3% in April, and averaged 33% for the 12 months ending February 2021. Demand was reduced by 59%, and rates were slashed in half, resulting in average RevPAR of $34.60.

click on image below to enlarge:

NOTE: Data is based on the 12 months ending February for each reporting year. Based on total rooms inventory: all temporarily closed hotel rooms supply calculated as if they were open.

Source: STR, compiled by Pinnacle Advisory Group, West.

The shelter-in-place order continued to be in effect until the end of May 2020, but by then, the tech companies of Silicon Valley had figured out a gameplan for maintaining productivity during the pandemic.

In mid-May 2020, Google and Facebook announced employees would be allowed to work from home for the remainder of the year. By the end May, 95% of Facebook’s employees were working off-campus. By early November 2020, all of Alphabet’s 200,000 employees and contractors were working off-campus, and they are expected to continue to do so until June 2021.

However, hardware-centric companies such as Apple had announced their slow phasing in of employees back into the office. These tech companies had redesigned their offices to provide one-way routes through the office, staggering work-stations, and limited in-person meetings as they had planned a “working during COVID” environment.

In January and February of 2021, the Valley sold an average of 302,800 hotel room nights, up from an average of 181,100 from March to June of 2020. Slowly, demand is improving.

Long term, Facebook has even predicted that 50% of its workforce will work remotely within the next 10 years. As Facebook continues to hire new employees, many have been in remote positions in areas surrounding existing offices to create hubs in geographically dispersed locations across North America. Twitter and Square offered permanent work-from-home options to employees. Zapier, a Silicon Valley startup even offered tech workers a $10,000 stipend to leave the Bay area and work remotely. Google is betting that some combination of remote and office work will predominate and announced this month that they are investing $1 billion in California, including the expansion of their Mountain View headquarters.

Much has been published on a recent exodus of tech workers from the Bay Area, but this seems to be exaggerated. A recent analysis of the U.S. Postal Service’s change of address notices indicated that there was a net loss of 53,000 households from the City of San Francisco. However, about 28,000 of those households moved to another Bay Area county, which means a net loss of 25,000 households — only 0.7% of total households.

It is not known yet if the moves by Oracle and HP’s Business Enterprise division will turn this trickle into a stream or river. Will there be other employers? The Bank of Silicon Valley tracks venture capital fundraising and observed that venture capital firms are sitting on enough cash to fund one and a half years of investment at the long-term average spend level. Nearly $160 billion was raised in 2029, which is a record high.

But where will these jobs and this hotel demand be created? Bank of Silicon Valley also tracks that. The Raleigh, Austin and Nashville markets appear very attractive in most metrics, with the exception of tech talent.

Venture capitalists have been on a spending spree, investing in Raleigh-based tech startups at a three-year compound annual growth rate of 36%. Washington, D.C., is the second-hottest area, where tech investment has been growing at a compound annual growth rate of 16%, followed by Denver and Nashville both at 12%.

The thing about percentages is that it is easier to show high numbers on a small base. The Bay area, with the preponderance of tech jobs, is still turning in a respectable 8.% compound annual growth rate in venture capital investments. Only in the tech world is an 8% compound annual growth rate a small number. The Silicon Valley is to tech what Los Angeles is to entertainment and New York is to finance.

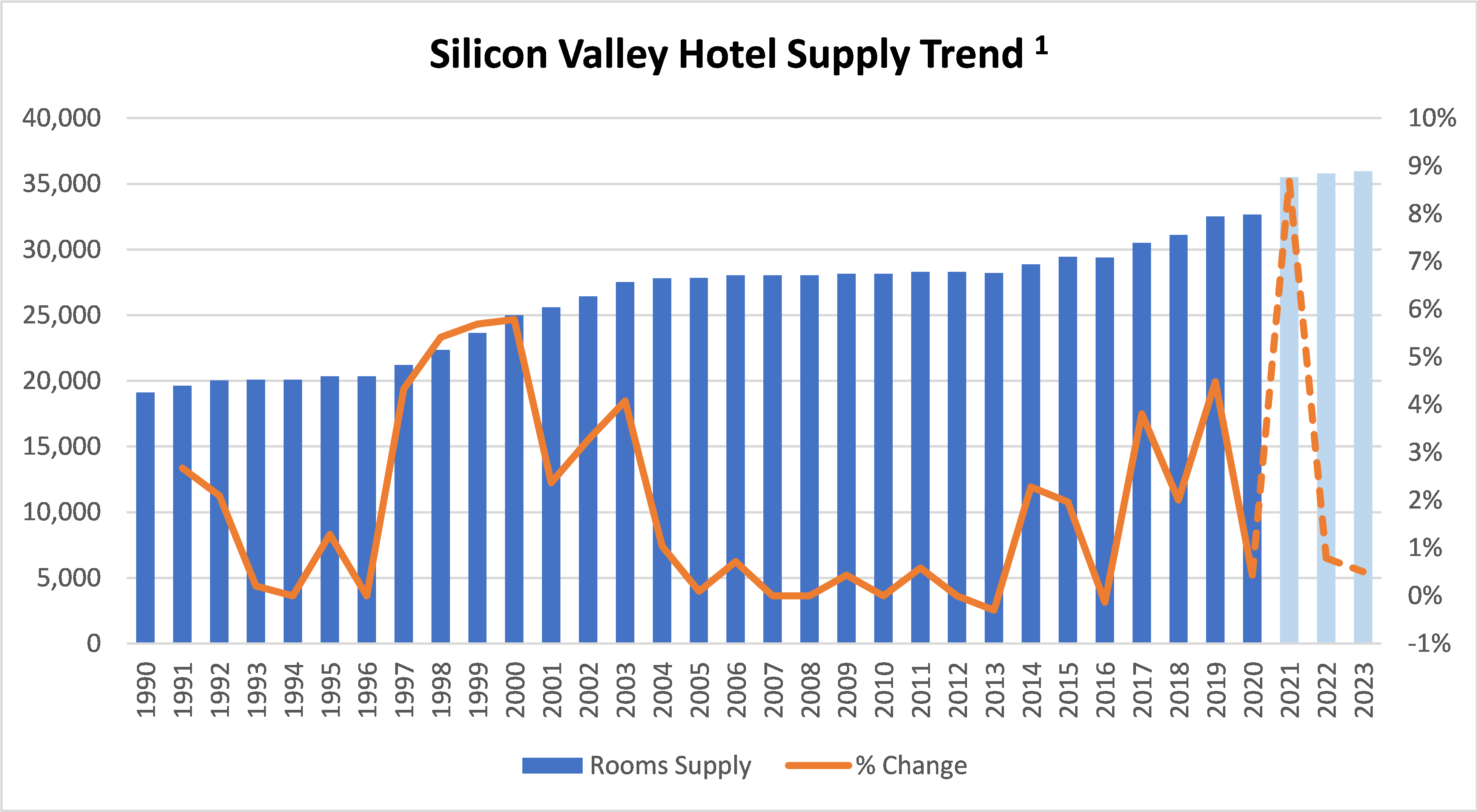

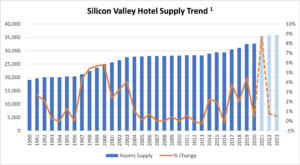

While waiting for the market to recover, however, existing hoteliers will also have to contend with the 18 hotels, totaling 3,100 rooms, currently under construction. Many slated to open in 2020 were delayed, and the vast majority of those rooms are currently slated to open this year. If the announced openings occur, supply will grow by 8.7% by the end of the year — twice the recent year’s average.

click on image below to enlarge:

1 This table includes only hotels under construction, not include projects in planning.

Source: STR, Pinnacle Advisory Group West

The Silicon Valley is a corporate market, with little weekend demand. Its largest employers set travel norms for smaller employers. The pace of recovery in the Silicon Valley will be determined by the tech giants’ relaxation of travel prohibitions, which may change with vaccination progress. The medium- and long-term prognosis is good. At present however, it appears hoteliers are due for another miserable year.

March 23, 2021 1:33 pm

Comments Off on Boston & Cambridge Lodging Market Update – GBCVB Venue & Attraction Meeting On March 23rd, Sebastian Colella presented to the Greater Boston Convention & Visitors Bureau’s (GBCVB) members in the venues and attractions industry. The presentation provided an overview of the Boston and Cambridge Lodging Market; what transpired in 2020 as a result of the pandemic, how it was impacted comparative to other major markets, and what can be expected from a recovery in the near and long-term. Attendees included representatives from local sports teams, meeting and event venues, museums, colleges and universities, restaurants, and other tourist attractions – all of which are directly and indirectly tied to the local hotel community.

Click on the link below to view presentation:

GBCVB Meeting 3.23.21

February 3, 2021 4:08 pm

Comments Off on Boston and Cambridge Lodging Market Update presented to the GBCVB – by Sebastian Colella Sebastian Colella presented the Boston and Cambridge Lodging Market update to the GBCVB. This presentation includes a review of 2020 data and an outlook for 2021.

Click below to view the presentation:

GBCVB Lodging Market Update 2.2.21

January 20, 2021 10:20 pm

Comments Off on Amidst Near-Term Headwinds, the Boston & Cambridge Lodging Market Awaits Recovery – by Sebastian Colella With large increases to its rooms supply and a heavy reliance on corporate and group travel, the Boston market faces an uphill battle in its recovery.

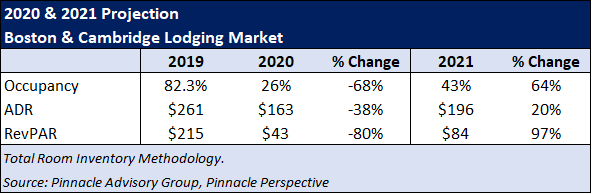

The travel and leisure industry has finally wrapped up 2020; a year like no other, with hotels enduring devastating declines to demand and revenue, job losses across the industry, government restrictions to day-to-day business, and extreme levels of uncertainty. As the United States faces a growing number of COVID-19 cases, surpassing 20 million by year-end 2020, lodging markets across the country continue to face unprecedented declines in demand. The Boston & Cambridge lodging market’s demand, or occupied roomnights, declined approximately 68% in 2020 when compared to 2019. Following its worst performance on record, the market is poised for growth in 2021 but faces an uphill battle to recovery in the short-term.

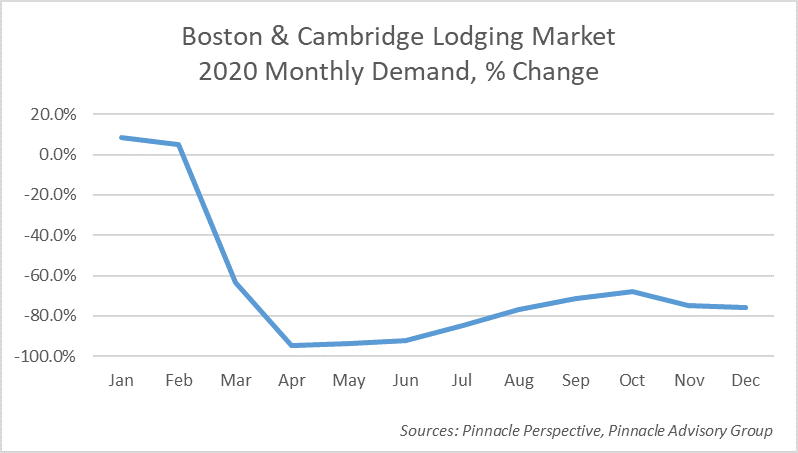

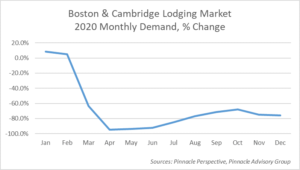

2020, The Market’s Worst Year on Record

Although the year began with increases to demand in January and February, things changed dramatically in March as COVID-19 case numbers increased and a State of Emergency was declared by Governor Baker resulting in a decline of lodging demand of over 60%. Between April and June, the Boston & Cambridge market experienced demand declines of over 90%. These declines improved during the summer and fall months as the State began its phased reopening allowing regional leisure demand to increase. However, November and December, historically the slowest months for the market, experienced further declines in demand as case numbers began to surge ending the year with demand declines of approximately 75%.

click on image to enlarge:

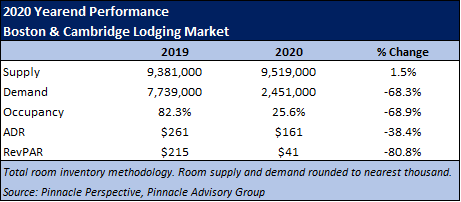

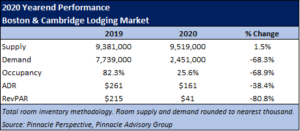

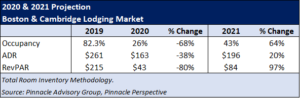

Using the total room inventory methodology which assumes no temporary closures, the Boston & Cambridge lodging market had an occupancy of 25.6%, a considerable decline from the 82.3% occupancy achieved in 2019. Relying primarily on lower rated leisure and contract demand through much of the year, the market’s ADR declined over 38%. With a revenue per available room (RevPAR) of $41, owners and operators in Boston and Cambridge have generated approximately 81% less room revenue than the prior year.

click on image to enlarge:

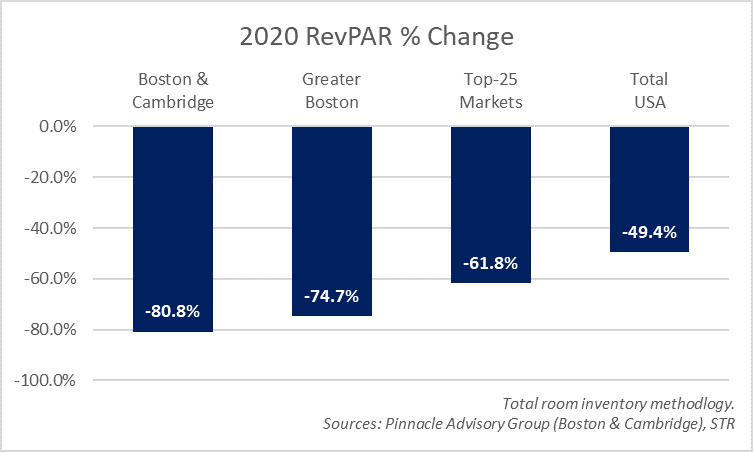

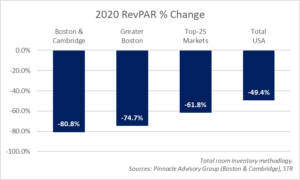

Gateway markets with a large amount of international travel, and urban markets which historically have a considerable amount of group and corporate demand, have been the most impacted by the ongoing pandemic. Not only does the Boston market meet these criteria, but it was also one of the early epicenters of coronavirus cases and one which had severe government restrictions to businesses and large gatherings. According to STR, RevPAR in the Greater Boston Market declined 74.7% compared to the prior year, a decline second to only New York City. As outlined below, the Boston & Cambridge market’s RevPAR decline in 2020 was more severe than the Greater Boston market, the Top-25 Markets in the US, and the country as a whole.

click on image to enlarge:

2021, What Lies Ahead

Through the first two weeks of the year, case counts show little sign of slowing both nationally and in Massachusetts. The year began with over 20% of the Boston & Cambridge rooms supply either closed or converted to dormitories for local colleges and universities. The hospitality and leisure industry represents one in ten jobs in Massachusetts and, as of November 2020, was down 35% compared to the year prior. Vacancies in the Boston and Cambridge office and lab market increased from 7.1% to 12.0% compared to the same time last year, the largest increase since the tech bubble. It is still unknown how the economic environment will change moving forward, however most owners and operators are aware of the long recovery ahead but are cautiously optimistic that it will begin to materialize in 2021.

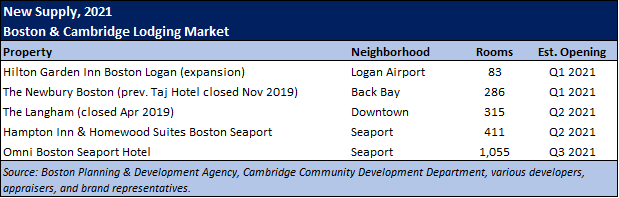

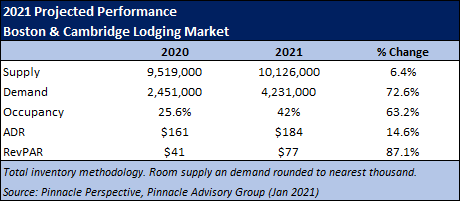

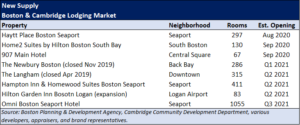

Among the headwinds facing the Boston & Cambridge lodging market is an increase to rooms supply. As market demand begins to recover, especially through the second half of 2021, the market’s room supply will expand at its largest rate in over 20 years. With five additions to the market in 2021, the number of available rooms is expected to increase 6.4%, utilizing the total rooms inventory method.

click on image to enlarge:

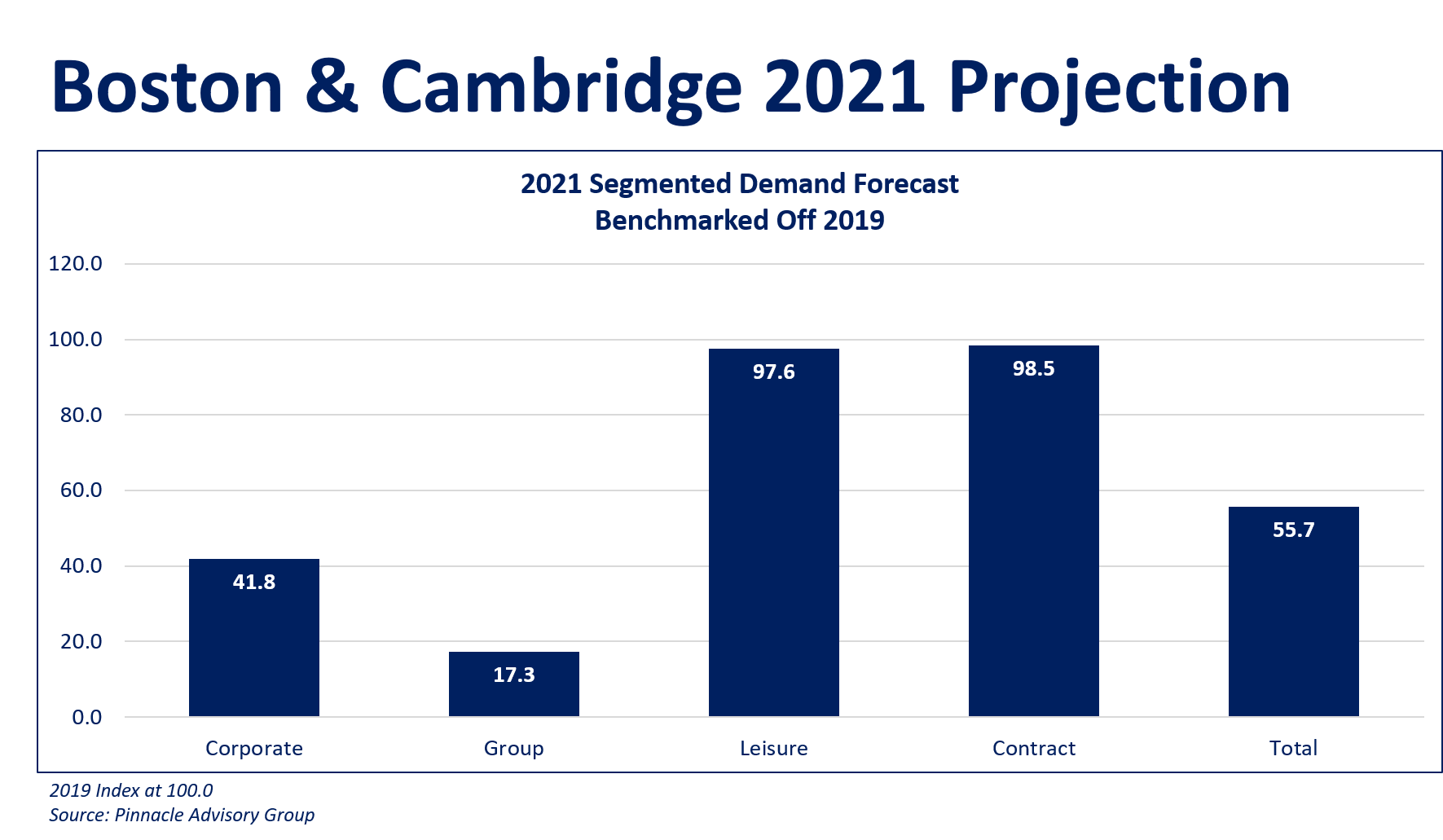

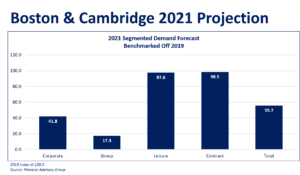

Historically, lodging demand in the Boston & Cambridge market has been consistently split among corporate transient, group, and leisure, each representing about 30-35% of total demand. The pandemic shifted this mix greatly in 2020 as corporate and group demand were diminished for practically ten months of the year. Given the anticipated improvement to travel that will result from the implementation of a national and world-wide vaccine program which has recently begun, Pinnacle Advisory Group’s outlook for each demand segment is outlined below.

Corporate: Given the shift to work remotely in 2020 and very little corporate travel, both domestic and international, there has been a considerable decline in corporate lodging demand in the Boston market since March. According to a number of local operators, there was a slight increase in corporate demand in September and October, however this began to diminish mid-November. We have forecasted the corporate segment to begin its recovery in Q2 2021, with increased growth rates through the second half of the year. A widely distributed vaccine and a federal response to liability protections will help to encourage corporations to expand travel. Our 2021 projections reflect the corporate segment reaching approximately 50% of 2019 levels by yearend.

Group: One of the most impactful government restrictions to the lodging market has been the guidance on large gatherings. As a result of the orders, the last event held at one of Boston’s convention centers was in March 2020 and there has been very little group and convention demand in the market since. Outside of small SMERF (Social, Military, Education, Religious and Fraternal) groups which are typically low rated, hotels have not had the benefit of hosting groups. We have forecasted this trend to continue through the first half of 2021. The recovery of the group segment will depend largely on when restrictions to travel and large gatherings are eased or lifted, or ultimately when an effective vaccine is widely available. The booking window for the group segment is by far the longer, often times booking larger events over a year in advance, or citywide conventions five to seven years in advance. For this reason the group segment will take longer to recover fully. As of January, the city’s two convention centers and many full-service hotels have a significant amount of group demand on the books as early as Q2 2021. Our 2021 projections reflect the group segment being approximately 30% of 2019 levels by yearend and assumes that although attendance may be less than originally anticipated, events currently scheduled for the second half of 2021 will take place.

Leisure: On the rise through much of the summer and fall months, leisure demand was made up of mostly regional travelers. This segment is expected to ebb and flow with seasonal swings, holidays and vacation periods, or driven by local demand generators. Our 2021 projections reflect the leisure segment reaching approximately 80% of 2019 levels by year-end. With very little corporate and group demand in the market, leisure rates are expected to be extremely competitive.

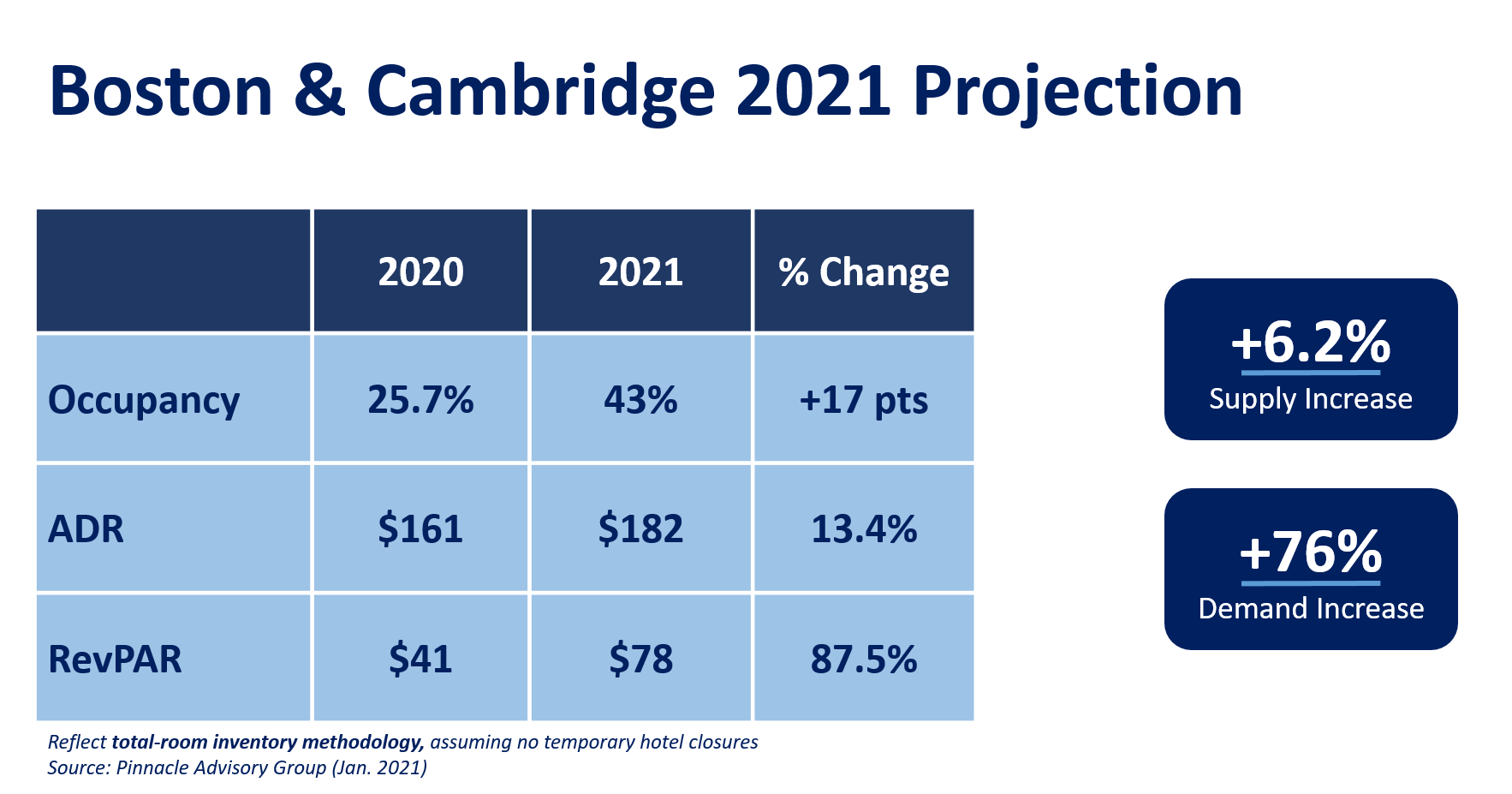

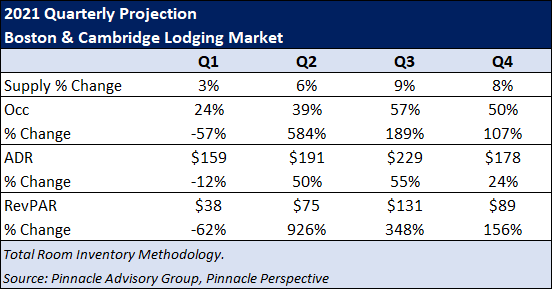

Pinnacle Advisory Group utilizes a Total Rooms Inventory (TRI) methodology which assumes all hotel rooms are available and operational, including rooms which are temporarily closed or being used as student housing. Pinnacle Advisory Group has projected demand in the Boston & Cambridge lodging market to increase approximately 73% in 2021, equating to a 42% market occupancy. Although the market’s ADR recovery is expected to take longer than occupancy, Pinnacle has projected ADR to increase approximately 15% in 2021, the majority of which will be realized in Q3 and Q4.

click on image to enlarge:

While reported progress in vaccine development is welcome news, especially to industries which rely on travel and leisure, there remain numerous unknowns as to when and how the global economy will return. As outlined, we believe after a fairly weak first half to 2021, economic growth will materialize in the third quarter. Pinnacle has forecasted the Boston & Cambridge RevPAR to reach pre-pandemic levels in 2024. Certain submarkets may take longer, specifically those which rely more on group demand, international travelers, or those which will see above average increases to supply during the recovery period. Alternatively, well branded, value-oriented hotels which rely more on leisure travel will be well positioned the next few years, as will submarkets which rely on stable demand generators such as the market’s many healthcare institutions.

Although the overall market’s recovery may to take longer than other top-25 markets, the Greater Boston economy is built around education, healthcare, high-tech research, and financial services all of which have proven to contribute greatly to the lodging market. These stable economic drivers, matched with a highly skilled workforce, a robust tourism and convention destination, and the strength of Boston Logan International Airport, position the Boston lodging market well for a recovery once the country begins to emerge from the pandemic.

Sebastian J. Colella is a Vice President with Pinnacle Advisory Group based in the Boston office. With over 20 years in the hospitality industry, Mr. Colella leverages his operational knowledge and expertise from experiences in the field. Work with Pinnacle Advisory Group has included market and feasibility analysis, acquisition due diligence, departmental revenue and expense performance evaluations, facility recommendations, brand assessments and impact studies, as well as appraisals of both branded and independent hotels and resorts. Sebastian is an adjunct professor at the Boston University School of Hotel Administration and received his bachelors of science degree at the School of Hotel Administration at Cornell University.

December 14, 2020 9:22 pm

Comments Off on Boston & Cambridge Hotels Choose Dormitories over Dormancy – by Sebastian Colella Article featured in Banker & Tradesman, November 30, 2020

The Boston & Cambridge lodging has ranked as one of the best performing markets in the country the last few years. Market occupancy was 82.3% in 2019, the seventh consecutive year above 80%. However, as a result of the ongoing pandemic and its impact to the Greater Boston economy, the market has faced some of the steepest declines in demand and revenue across the country’s top-25 markets according to STR. Although most hotels in the market have reopened after closing temporarily in the second and third quarters, they have done so with very little lodging demand. Given the challenging operating environment hotels have had to rely on some business it would not have considered in the past.

Greater Boston is home to over 50 colleges and universities, including Harvard University, the Massachusetts Institute of Technology, Boston University, and others, which is more than any other metropolitan area in the country. As these schools prepared to welcome back students and staff during the ongoing pandemic, many were forced to de-densify accommodations and provide additional housing for quarantining and testing. Given the lodging market’s performance the last ten years, it is unlikely hotel owners and operators in the Boston market would have considered providing room blocks at substantially discounted rates to schools for an extended period of time. However, the proposition has been viewed as a win-win for about a dozen hotels given the dramatic declines in lodging demand this year.

The majority of hotels in Boston and Cambridge temporarily closed in March or April, with an estimated 80% of the rooms supply closed in May. Although most hotels have since reopened, ten hotels remain closed representing approximately 12% of the market’s room supply, including the market’s largest hotel, the 1,220-room Sheraton Boston. In addition to these hotels closing to transient and group demand, hotels have offered up rooms to the universities and colleges for dorm use, removing even more room inventory from the market.

The needs vary by school and as such the contracts with each hotel can vary greatly from the nightly rate to the hotel services provided. Based on conversations with these hotels, Pinnacle estimates approximately 1,400 rooms being used nightly for this purpose, equating to approximately 5% of the market’s current supply. The average daily rate (ADR) for these contracted rooms is approximately $100, less than a third of the market’s ADR in October 2019. Half of the contracts run through the first semester, ending mid-November, while the other half extend through the spring semester to May or June. Given the length of these contracts and that they are contracted with tax exempt schools, the room revenue is not subject to state or local lodging tax.

Although these students are not receiving the typical college experience, they are being housed in some of the city’s nicest hotels, many of which are branded, full-service hotels which have implemented elevated cleaning standards. With occupancy levels as low as they have been this year, these hotel rooms would have most likely gone empty. Agreements with the colleges have enabled hotels to generate some level of income during Q3 and Q4 of this year while also bringing some furloughed employees back to work. If demand remains at these levels, hotel owners will continue to seek out college and university dorm agreements as one way to generate revenues.

Pinnacle Advisory Group’s projections for 2020 and 2021 are outlined below.

Click on image below to view larger:

While reported progress in vaccine development is welcome news, especially to industries which rely on travel and leisure, there remain numerous unknowns as to when and how the global economy will return. As a destination and as an economy, the Greater Boston area is built around education, healthcare, high-tech research, and financial services all of which are equally stable and strong demand drivers. Matched with a highly skilled workforce, robust tourism and conventions, and the strength of Boston Logan International Airport, the market is well positioned for a recovery once the country begins to emerge from this pandemic. Until this time, both hotels and colleges will benefit from the use of hotel rooms as dormitories.

Sebastian J. Colella is a Vice President with Pinnacle Advisory Group based in the Boston office. Sebastian has over 15 years of experience in the hospitality industry.

Pinnacle Advisory Group. Founded in 1991, Pinnacle Advisory Group is considered to be one of the top hospitality consulting, advisory, and asset management firms in the country. Since inception, Pinnacle has provided advice on more than $50 billion of hotel real estate. The Pinnacle team consists of some of the hospitality industry’s most seasoned professionals. Pinnacle’s services include asset management, feasibility studies, workout strategies, acquisition due diligence, litigation support, appraisal and valuation, operational reviews, operator/franchise selection and contract negotiations, financial diagnostics with sensitivity analysis, and other advisory support to hotel owners and lenders. (www.pinnacle-advisory.com)

November 17, 2020 9:50 pm

Comments Off on Lodging Recovery in Boston & Cambridge Driven by Leisure Demand as Market Faces Increases to Supply – by Sebastian Colella As the United States faces a growing number of COVID-19 cases, surpassing 10 million in early November, lodging markets across the country continue to face unprecedented declines in demand. Through October, the Boston & Cambridge lodging market has experienced some of the steepest declines in demand and revenue across the country’s top-25 markets according to STR. Now operating in the winter season, historically the slowest demand period for the Boston & Cambridge market, increasing case numbers have resulted in further restrictions to travel, gatherings, and businesses which were eased over the summer months. The pandemic’s impact to demand continues to reshape the room supply in the Boston & Cambridge market and while there have been improvements to demand levels since the spring, the road to recovery will be long.

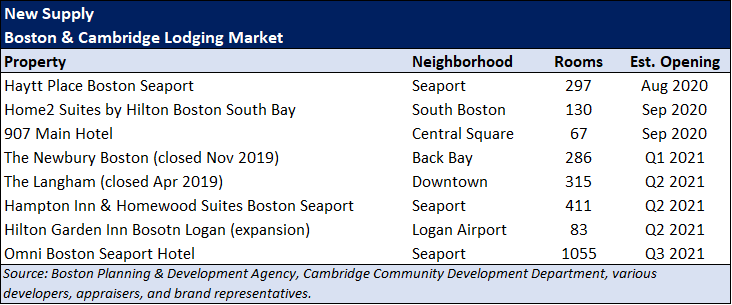

The majority of hotels in Boston and Cambridge temporarily closed in March or April, with an estimated 80% of the rooms supply closed in May. Although most hotels have since reopened, ten hotels remain closed representing approximately 12% of the market’s room supply, including the market’s largest hotel, the 1,220-room Sheraton Boston. Additionally, approximately 5% of rooms supply has been contracted to local colleges and universities for use as student housing. Based on conversations with multiple hotel operators, a number of hotels will temporarily close again with tentative reopenings planned for the spring, while others have already reduced operations to weekend nights only. These reductions to supply are occurring concurrently with new additions; three new hotels opened in 2020 combined for approximately 500 rooms, a 1.5% increase to market supply.

click on image below to view:

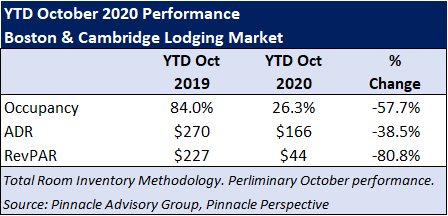

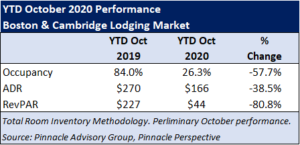

Through October, the Boston & Cambridge lodging market’s demand, or occupied roomnights, has declined over 68% when compared to the same time last year. Although the market was experiencing demand declines of over 90% between April and June, these declines have improved during the summer and fall months. As a result, the market occupancy is slightly over 26% through October, a considerable decline from the 84% occupancy achieved last year through October. Relying primarily on lower rated leisure and contract demand, the market’s average daily rate (ADR) has declined 38.5% during the period. With a revenue per available room (RevPAR) of $44 through October, owners and operators have generated 80% less room revenue than the prior year.

Historically, lodging demand in the Boston & Cambridge market has been consistently split among corporate transient, group, and leisure, each representing about 30-35% of total demand. Pinnacle Advisory Group’s outlook for each segment is outlined below.

- Given the shift to work remotely this year and very little corporate travel, both domestic and international, there has been a considerable decline in corporate lodging demand in market since March. According to a number of local operators, there was a slight increase in corporate demand in September and October. Despite these minor increases, Pinnacle expects corporate demand levels to begin to diminish in mid-November. We believe that the corporate segment will begin to recover in Q2 2021, with increased growth rates through the second half of the year. Our 2020 and 2021 projections reflect the corporate segment reaching approximately 25% and 50%, respectively, of 2019 levels by yearend.

- One of the most impactful government restrictions to the lodging market has been the guidance on large gatherings. As a result of the orders, the last event held at one of Boston’s convention centers was in March 2020 and there has been very little group and convention demand in the market since. Outside of small SMERF (Social, Military, Education, Religious and Fraternal) groups which are typically low rated, hotels have not had the benefit of hosting groups. We have forecasted this trend to continue through the first half of 2021. The recovery of the group segment will depend largely on when restrictions to travel and large gatherings are eased or lifted, or ultimately when an effective vaccine is widely available. As of November, the city’s two convention centers and many full-service hotels have a significant amount of group demand on the books as early as July 2021. Our 2021 projections reflect the group segment reaching approximately 15% of 2019 levels by yearend and assumes that although attendance may be light events in the second half of 2021 will take place.

- Leisure demand was on the rise through much of the summer and fall months. Made up of mostly regional travelers, this segment is expected to ebb and flow with seasonal swings, holidays and vacation periods, or driven by local demand generators. Our 2021 projections reflect the leisure segment reaching approximately 70% of 2019 levels by year-end. With very little corporate and group demand in the market, leisure rates are expected to be extremely competitive.

As market demand begins to recover through much of 2021, the Boston & Cambridge market’s room supply will expand. With five additions to the market in 2021, the number of available rooms is expected to increase 6.7%, its largest increase since 1999. Hotels entering the market in 2020 and 2021 are outlined below.

click on image below to view:

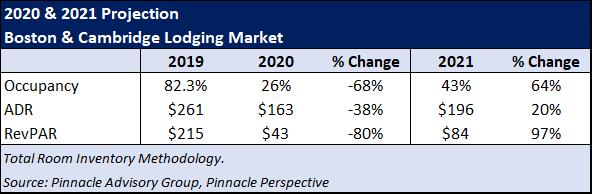

Pinnacle Advisory Group utilizes a Total Rooms Inventory (TRI) methodology which assumes all hotel rooms are available and operational, including rooms which are temporarily closed or being used as student housing. Pinnacle Advisory Group has projected demand in the Boston & Cambridge lodging market to decline 68% in 2020, equating to a 26% market occupancy. ADR is expected to decline 38%, resulting in a decline in RevPAR of over 80% when compared to last year. As outlined previously, demand is projected to improve through 2021 achieving an occupancy of 43%. Although the market’s ADR recovery is expected to take longer than occupancy, Pinnacle has projected ADR to increase 20% in 2021, the majority of which will be realized in Q2 and Q3.

click on image below to view:

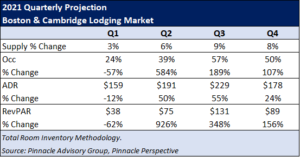

Quarterly projections for 2021 are outlined below.

While reported progress in vaccine development is welcome news, especially to industries which rely on travel and leisure, there remain numerous unknowns as to when and how the global economy will return. As a destination and as an economy, the Greater Boston area is built around education, healthcare, high-tech research, and financial services all of which are equally stable and strong demand drivers. Matched with a highly skilled workforce, robust tourism and conventions, and the strength of Boston Logan International Airport, the market is well positioned for a recovery once the country begins to emerge from this pandemic and long-term economic stability.

Pinnacle Advisory Group has updated its Boston & Cambridge Outlook originally presented in August 2020. This presentation which outlines market projections and trends for 2020 and 2021, can be found here.

6:17 pm

Comments Off on Revised Boston & Cambridge Outlook 2021 – by Rachel Roginsky, ISHC, and Sebastian Colella Pinnacle Advisory Group has updated its Boston & Cambridge Outlook originally presented in August 2020. This presentation outlines market projections and trends for 2020 and 2021.

Click on the link below to view presentation:

Revised Outlook 2021 11.17.20

November 4, 2020 9:03 pm

Comments Off on Bad vs Horrible – Depends on How Performance is Measured. by Allison Fogarty The importance of considering Total Rooms Inventory (TRI) in measuring Lodging Industry performance.

Through the pandemic, hotel Occupancy rates have hit historic lows throughout the country. We have constantly been asked “how bad is it?” Reports early in the pandemic, while awful, seemed to actually understate the catastrophic effect of the pandemic on the hospitality industry. We studied figures provided by STR and other industry analysts and questioned their representatives to fully understand reporting methodologies in an effort to truly understand the current situation in the lodging industry.

Unfortunately, the industry’s standard measure of capacity utilization – Occupancy – is traditionally based on the number of available rooms in a market divided by the number of occupied rooms. This standard methodology is based only on hotels that are open and operating, so if hotels have been closed either due to government restrictions or lack of guests rendering operation uneconomic, rooms at temporarily closed properties are removed from the inventory of available rooms.

Earlier this year I, along with my colleagues at Pinnacle Advisory Group, was puzzled when occupancy levels in some local Florida markets – Miami and Orlando in particular – were higher than expected given the cities’ dependence on mass tourism and conferences. The mystery was solved when I realized that hotels that had closed were not included in standard occupancy statistics. Additionally, in some markets where new hotels have been added during the pandemic, the supply and demand picture is further complicated. In the standard occupancy calculation, temporary closures disguise the true impact of additions to supply during the pandemic, as permanent supply increases may be masked by offsetting temporary closures.

STR, the lodging industry’s statistical data guru, recently began to provide an alternate occupancy measure based on the Total Rooms Inventory (TRI) in a market, which counts temporarily closed rooms as part of the denominator, reducing Occupancy. In general, the percentage difference in Occupancy between the two Occupancy calculation methods is the same as the percentage difference in supply between the two methods. As properties reopen (or close permanently), the standard and TRI occupancies will trend together.

Standard occupancy calculations make sense in benchmarking individual properties, as hotel managers should compare their hotels against other open properties. For analysts concerned with the bigger picture, and those that are trying to determine when it may be worth re-opening, the analysis is more nuanced. Total Rooms Inventory (TRI) Occupancy allows corporate staff and analysts to understand the true supply and demand picture, as presumably when the market returns to “normal”, many of the temporarily closed rooms will reopen, competing for available demand.

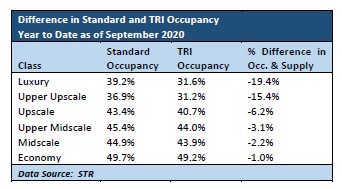

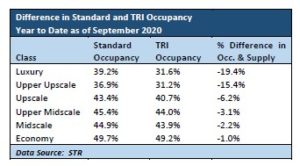

Luxury and upper upscale properties, many of which are reliant on group demand, are overrepresented among closed properties nationwide. On a year to date basis as of September 30, over 19% of luxury rooms, and over 15% of upper upscale rooms were closed during the first nine months of the year, while only a small percentage of economy rooms were shuttered. Many hotels have reopened, but 11.7% of luxury and 12.0% of upper upscale hotels remained closed in September. The flowing chart highlights the difference between standard and TRI Occupancy measures, and hence the percentage of rooms closed by hotel classification.

click on image to enlarge:

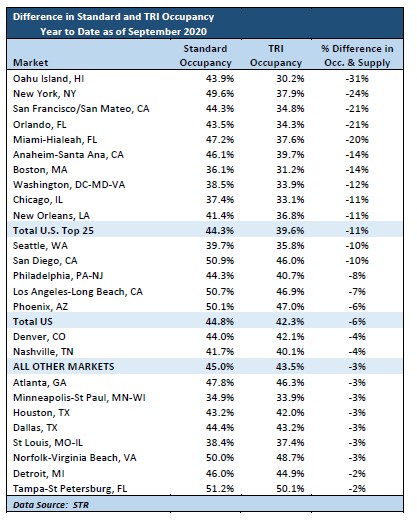

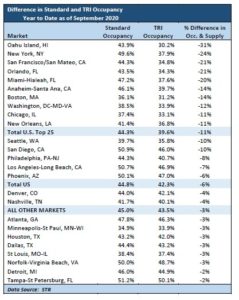

Closures have unequally affected markets across the country. Cities known as the first epicenters of the pandemic (including New York, Miami and Boston), large convention destinations (such as Chicago, Orlando, and New Orleans) and cities reliant on air-based leisure travel (Oahu and Orlando) have among the most significant discrepancies between standard and TRI occupancy. Based on STR figures as of September year to date, of the nation’s top 25 markets, Oahu Island, Hawaii had the largest discrepancy between the two occupancy measures and hence the greatest percentage of closed hotel rooms, while Tampa Bay, Florida had the fewest shuttered rooms. Among the nation’s top 25 markets, New York, Orlando, and San Francisco had the most shuttered hotel rooms, while Norfolk -Virginia Beach is the only top 25 market where all hotels are reportedly open.

The following chart details the difference in year to date occupancy between standard occupancy measures and the TRI occupancy when all the rooms in the market, including those that are temporarily closed are counted.

click on image to enlarge:

“How bad is it?” Well, its bad all over, but in some of the smaller markets: the Tampa Bay area, Detroit, and Norfolk/Virginia Beach, as of September, most rooms in the market were open, and the TRI RevPAR decline was lower than the national average of 49.5%. In other major markets, including New York, San Francisco, Chicago and Boston, a significant percentage of the supply is currently off the market, and TRI RevPAR has declined by over 65%, indicating that the path to normality is likely to be steep and bumpy as hotels in these markets reopen, diluting available demand.

About Pinnacle Advisory Group

Since 1991, Pinnacle Advisory Group has provided advice and analysis on the full spectrum of hospitality properties throughout the US and Caribbean in all phases of the economic cycle. Pinnacle’s services span investment advisory, market and financial feasibility analyses, valuation, litigation support, asset management services, receivership, development consulting, and strategic planning. Our clients include major banks, leading hotel companies, REITs, universities, and municipalities. Our seasoned professionals have diverse backgrounds encompassing operations, strategic planning, real estate appraisal, and consulting.

About the Author

Allison Fogarty is the Managing Director of Pinnacle Advisory Group’s Florida and Caribbean Practice Group. Ms. Fogarty has extensive experience in strategic planning, and financial analysis and operational oversight in the hotel industry. Her corporate activities have included site selection, property inspection, contract negotiation and review, and due diligence. As a consultant, she has directed and completed market and financial analysis engagements and investment counseling for hotels and resorts in the eastern United States and the Caribbean.